Inflation - hyped or underestimated?

TMC #3! Everybody and their mothers are talking about inflation. Let me shed some light on where I think we are going.

Inflation is primarily a monetary phenomenon: when too much money is chasing the same basket of goods, the price of this basket of goods goes up. And that’s called inflation. One might argue it’s also a behavioral phenomenon: consumers experiencing price increases might draw the conclusion it’s time to buy now rather than later, leading to a vicious spiral of self-feeding price increases.

Ok, stop with the boring definitions and get to the point.

The point is that we ARE going to see inflation over the next 3-4 quarters. To the tune of 4% on average or so in the US: wow, that’s big. But it’s already priced.

What’s also priced is that these 4% inflation prints are not sustainable. I agree.

A while ago on Linkedin I called for US Core Inflation to print >3% in a sustainable way. When you expand credit in a very quick fashion via gargantuan fiscal stimulus compared to the size of the output gap and you couple that with supply chain bottlenecks, what would you expect? Yes, inflation.

Back then, I showed the good correlation between household net disposable income YoY and core inflation YoY. The US fiscal stimulus sent the median US family disposable income up +8% on average between Mar 2020 and Mar 2021. The average between 2016 and 2020 was +2.5%. So, summing up:

2016 - end 2019

Average YoY household net income growth = +2.5%

Average core inflation YoY = +1.8%

Mar 2020 - Mar 2021

Average YoY household net income growth = +8% (stimulus checks)

Average core inflation YoY = ? (likely >3% for few quarters)

So, we must sell bonds right? This is unprecedented!

Wait a second, take one step back.

The point is you are not the only one talking about inflation: everybody is. There is nothing better than a collective price setting mechanism (i.e. financial markets) to find out how much this inflation narrative is discounted.

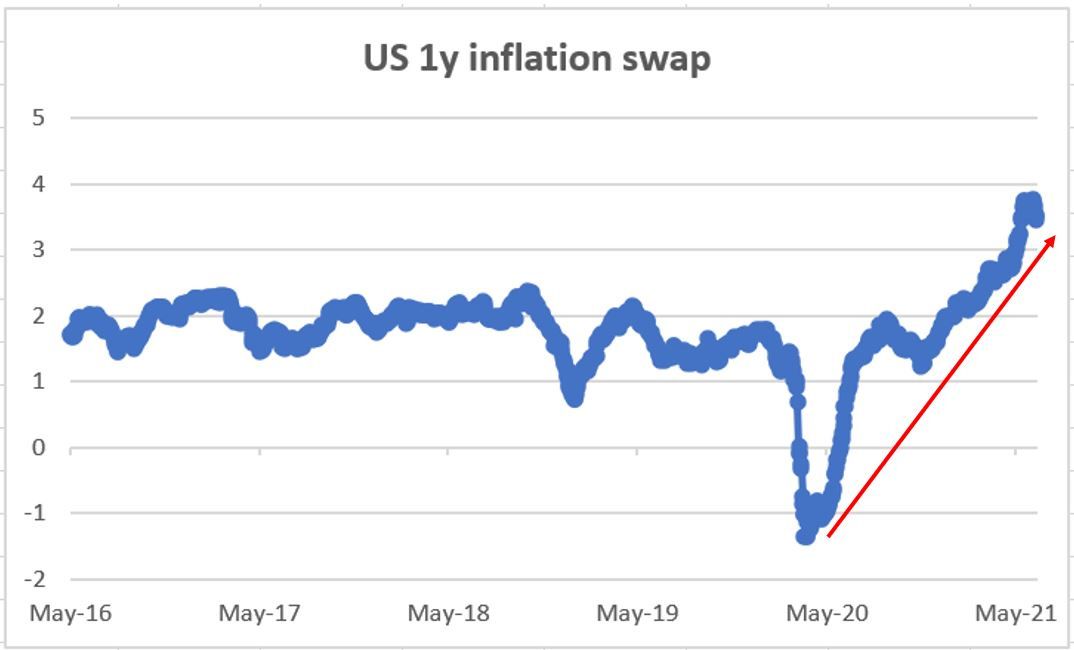

The chart below shows the US 1y inflation (CPI) swap. You agree to pay a fixed rate and receive a stream of variable payments based on where CPI will print between June 2021 and June 2022. The clearing level is now 3.63% - it’s mostly priced already.

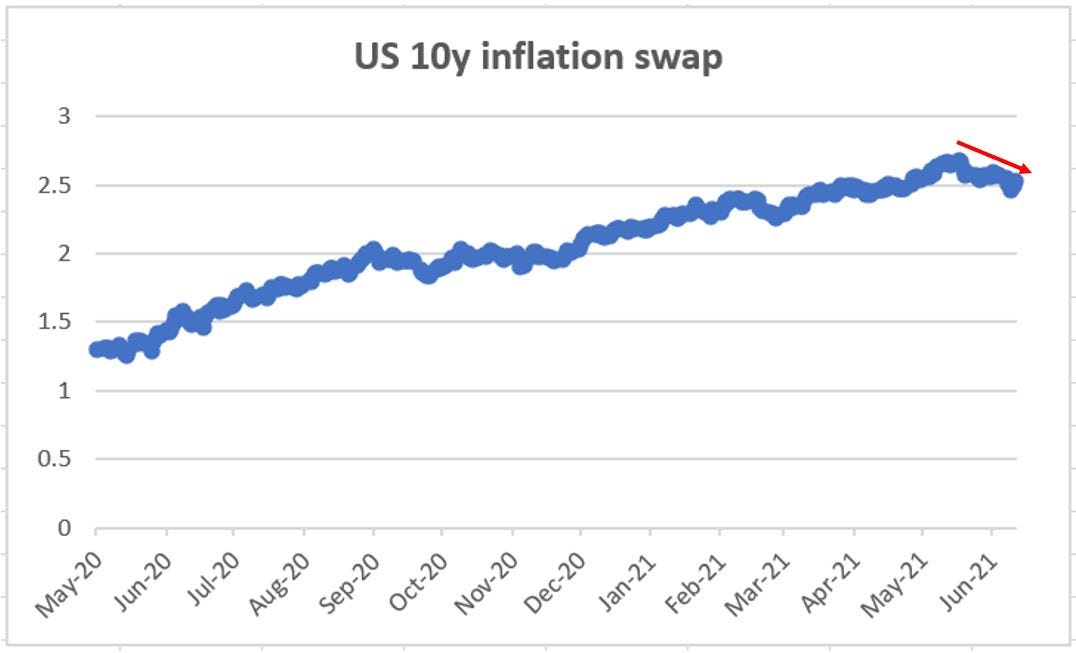

Now let’s take a look at US 10y inflation swaps and zoom in a bit to see what’s happening over the last few months in that market. Here you agree to pay a fixed rate and receive a stream of variable payments based on where CPI will print between June 2021 and June 2031. So, watch out, this is where inflation expectations are for the next 10 years, not for the next few quarters.

Eh? 2.5% on headline CPI and dropping from the highs? This would imply an average of 2%-ish core PCE (the Fed looks at this) for the next 10y despite the strong tailwinds of core PCE prints >3% for the next year or so.

Not quite the inflationary spiral. How come?

Well, fiscal sugar rushes always bring a fiscal cliff with them. Credit impulse has peaked already and it leads inflation expectations by about 8-12 months.

Supply bottlenecks are probably at their peak. Do you expect industries to never catch up with demand? And demand to always remain at the peak of reopening optimism? And workers never to re-enter the labor force?

Credit impulse leads inflation expectations very well. The more you slosh the private sector with newly created credit, the higher the chances this will lead to some form of short-term inflationary pressures.

In order to sustain these inflationary pressures, you need higher and higher credit impulse. Remember, that’s the change of pace of credit growth.

So now you’d need another fiscal stimulus even bigger than the 2020-early 2021 package. Yep, not gonna happen.

So, the market has probably smelled this. And it’s acting in a very coherent way.

Short-term inflation expectations are very high -> 1y US CPI swap at 3.6%.

Long-term inflation expectations have peaked -> 10y US CPI swap at 2.5% and dropping, implying core inflation to print at 2% on average for the next decade.

Up to you to decide on what to focus on: the prevailing short-term narrative or what the market is trying to tell you for the long-term?

Don’t miss the forest for the trees.

Did you like this post? Subscribe to this free newsletter for more updates.

Nice piece Alfonso! Very well written, easy to follow. Looking forward to the articles to come!

How do you calculate G5 credit impulse?