My approach to tactical and long-term investing

PA#1! A glance at the strategy I chose to invest my savings for the long-run and why I tactically turned bearish on the stock market.

By now, I assume you’re well aware of The Macro Compass and you have been so kind to share my global macro newsletter with your network.

If you are as lazy as I am, I hear you. Here is the share button below

Today we kick off the Portfolio Approach (PA) section, which I will use as my own investment diary for the tactical, discretionary calls I might put my money in.

I hope this makes TMC even more interesting.

Too many newsletters out there charging you for some non-actionable market views or even worse for market calls with no verifiable track record.

Instead, I’ll walk you through my up-and-down journey and will not hide my bad calls + refer only to the good trades (a very common practice…). It’s going to be as transparent as it gets. No cherry picking.

So, let’s start.

The tactical approach

The rules of the game are the following.

I invest long/short in global macro products with 10% of my savings. The bulk of my savings is invested in a long-term structural portfolio (more on that later).

Let’s call this 10% = 10.000 EUR as a starting amount.

The objective is to make >10% total return on this portfolio. At the end of the year, we will compare the return generated/risk taken versus the benchmark long-term structural allocation. Disclaimer: that b***h is hard to beat!

Every trade has a skewed stop/initial profit target: hard stop at -2.5% of remaining capital and initial profit target >2.5% (generally 1.5x or more). This way I can be right <50% of the times and still make money at year-end if I am thoroughly disciplined in hitting my stops.

The time horizon for trades is generally 1+ months.

In order not to hit stops too often, I place them at 1 standard deviation distance from today’s entry price calculated using 10y rolling monthly returns and assuming a normal distribution. The entry size is adjusted such that I can lose max 2.5% of my capital if that 1-sigma move hits me.

I will always cut my losses and let my profits run. The former is easy to understand. The latter means that if I hit my first profit target, I move it up by a bit and move up my new stop loss (now a profit target) by a bit. Profits keep on running until I hit my new stop (now a profit).

Yes I know, it’s not nearly a perfectly scientific approach and I am simplifying many things, but it should work as a general framework to try and see how my calls are doing.

Reminder: this is NOT investment advice. The above has to be interpreted as a public journal for a fictitious, paper portfolio. I always represent myself and not my employer.

Live trades:

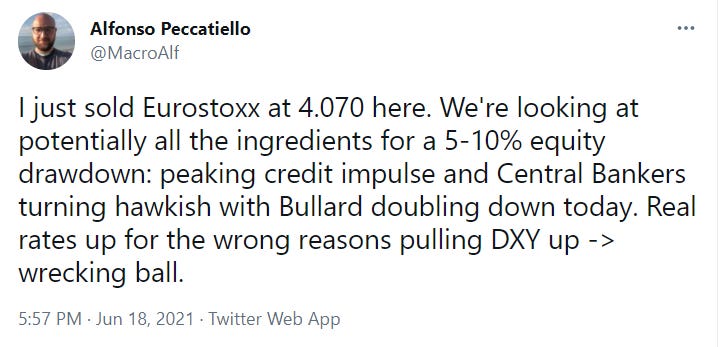

Jun-18: Short Euro Stoxx 50 @4.070, stop @4.275 (5%), first profit target @3.785 (7.5%).

Rationale:

Powell decided the overshoots in inflation needed to make up for undershoots in the past (AIT framework) were…just a couple of inflation prints at 4-5%. Aaaand we run for the hills already.

Bullard doubled down in an interview the day after. Kashkari tried to save the day but he’s so dovish that it’s hard to assign too much weight to his words.

The Fed has turned and does not stand firmly behind AIT. Tapering in September is highly likely and this monetary policy hawkish turn comes at the peak of the global credit impulse. 5s30s in US have noticed and started flattening aggressively: the bond market is implying lower future growth and inflation now, hence lower forward yields.

I am afraid we can have a good glance at Quadrant 4 for the next few weeks. All the ingredients are here to potentially experience a >5-10% equity drawdown, or at least I like the risk/reward of being short equities here.

The Euro Stoxx 50 was one of the DM stock market poster card for the reflation trade of Q420-Q121 due to its composition being skewed to financials and industrials.

Let’s see how this goes!

Ok, the tactical stuff - but what’s the long-run approach to investing my savings?

So, assume you live in Europe and you have accumulated 100k EUR in savings (wow man, well done). You look at the different asset classes and you’re like omg, that’s expensive. Wow, that other stuff is even more expensive.

I’d rather keep the cash and wait. Nothing wrong with that, right?

Well, that’s pretty much of an expensive decision even if it doesn’t feel like it.

In Europe, most bank accounts reward 0% nominal interest rate (soon: -0.50% above 50-100k savings threshold). The average annual rate of inflation over the last 7 years has been 1%. Negative real rate = -1%.

Let me show you what happened to the purchasing power of your savings by applying the ‘‘keep the cash and wait, nothing wrong with that’’ strategy.

Not that cheap of a choice anymore, is it?

The most important decision is not which stock to buy, how much gold you should own or what platform should you use to invest.

The most important decision is to get out of the stealth tax called ‘‘negative real interest rates’’ and start putting your money at work.

This gives you a decent chance to preserve or increase your purchasing power.

Idle money on a bank account provides you with the certainty to lose your purchasing power over time at negative real interest rates as we stand now.

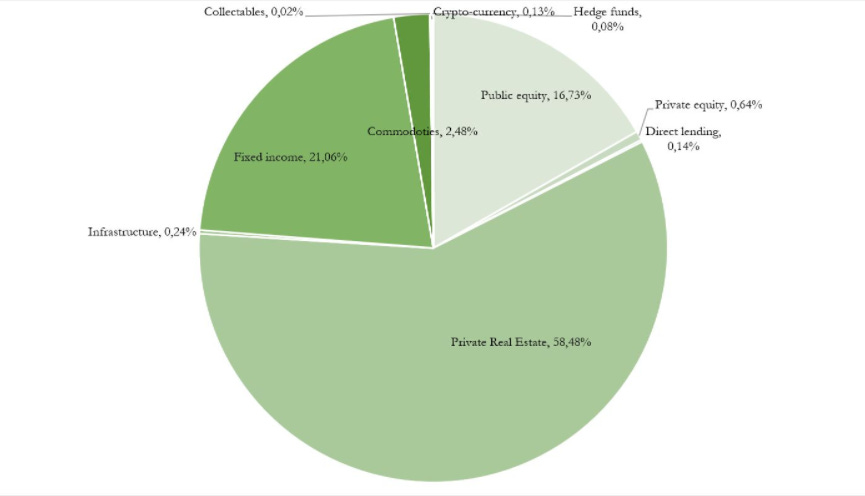

So now imagine there is one big investor in the world. This dude/lady congregates all the investment decisions made by every single little investor.

He owns the global market portfolio.

So, how does that look like today?

60% real estate, 21% fixed income, 17% equities, 2% commodities, 1% other stuff.

Notice, gotta zoom in to find crypto…

Anyway, who owns this exact portfolio? I guess the answer is almost nobody.

That’s why I don’t like the notion of ‘‘passive investor’’.

The sole action to get out of negative real interest rates makes you an active investor. Any allocation in macro asset classes different from the above chart also makes you an active investor.

Ok, so how does my long-term portfolio look like?

90% of my savings are invested in the portfolio below:

70% global equity, EUR hedged (e.g. ETF ticker: IWDE)

20% US Treasuries held in USD (e.g. ETF ticker: IBTM)

10% Gold (e.g. ETF ticker: PHAU)

The remaining 10% of my savings are allocated into a global macro tactical portfolio which I will document in the Portfolio Approach section of TMC.

Why this very simple choice of asset classes and allocations? After all, I am professionally involved in finance and hence I should be the guy punting in and out in fancy products, right? No. For a couple of reasons:

1) I want to be exposed to market beta returns. Alpha is very, very difficult to achieve. Not worth chasing it with the largest portion of my savings. I’ll try that with 10% of my savings and see what happens. Exposure to beta return should represent the bulk of my long-term strategic portfolio.

Here is a table showing the large percentage of active managers underperforming their benchmarks in equities. Over 10-20y, only 10% (maybe) consistently generate alpha.

2) The asset allocation and investment strategy for the bulk of your savings should be a non-stressful, easy process. No emotional swings involved. This makes it way easier to stick to a long-term plan.

The time spent in the market is way more important than timing the market.

Make sure you have a strategy that allows you to remain invested for the long run.

So, how did I come up with the 70-20-10 portfolio expressed above?

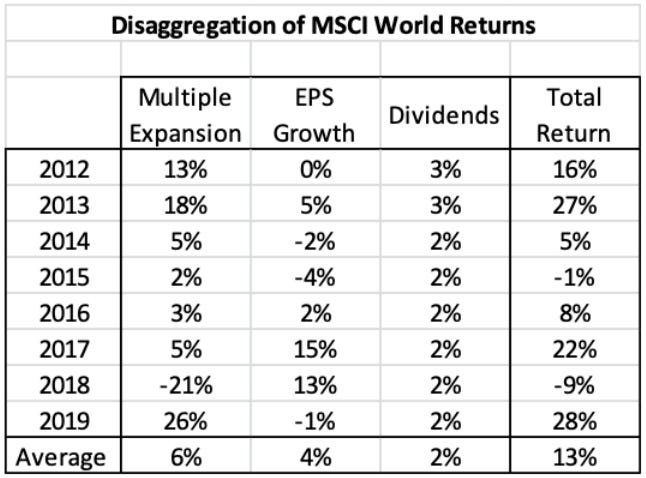

70% MSCI World, EUR hedged: global equities provide you with a great source of market (beta) returns as they are generally skewed to deliver positive returns over very long periods of times. Why?

Well, the total return of the equity market is the sum of dividends (DY) + delta in earnings (EPS) + delta in valuations (P/E). Guess what, DY is a positive number by definition and EPS growth tends to be positive over long periods of time. The P/E component provides the most volatile part of the total return, but the positive drift associated with DY+EPS generally works your way over long periods of time.

Here is a histogram of almost 200 years of US equity market returns.

Who am I not to own exposure to the most liquid source of asset returns which is positively skewed over long periods of time? And it works in real terms as well.

So, why not 100% in equities then?

Well, back to point 2. Investing 90% of my savings should be a non-stressful event. I need some defenders to reduce the inevitable drawdowns which I will face down to road to levels I deem acceptable not to freak out.

They defend against different risks, let’s see exactly what I mean.

US Treasuries denominated in USD represent one of the cleanest defenders against risk-off events for a European investor. The combination of safe asset and the USD denomination works well in stressed environments as investors rush for USD and USD-equivalent safe assets (mostly US Treasuries).

To make a long story short, the current global monetary system is way overleveraged in USD. The US alone is tasked to export the global reserve currency to all who need it and use it. Actually, that’s pretty difficult to achieve and hence the use of this weird thing called Eurodollar system: entities outside the US can borrow and lend USD (e.g. a European bank can make USD loans, a Latin American country can issue USD bonds).

All cool and dandy until the economy slows down and risk aversion takes place: the Eurodollar system breaks as lenders back off from providing USD and actually want to make sure they have access to USD liquidity - which can be provided by the Fed immediately for domestic entities. A bit more cumbersome for non-US entities.

As per 2019, there were 12 trillion (!) USD loans outstanding to non-US entities. When systemic risk aversion picks up, a rush towards USD denominated cash (or safe assets) is generally associated. Good defender.

Gold (10% weight) constitutes mainly a tail risk hedge against the implosion of the current fiat based monetary system. Today’s system allows us to expand our money supply in a totally elastic way, and this has led to us…doing exactly that.

This way we can overlay cyclical and temporary growth (via extending credit and borrowing from future growth) on the poor and declining structural growth. You make this generation happy by kicking the can down the road.

Now, if this system breaks the payoff function of different asset classes is very unlikely to be linear but it’d rather be convex.

Gold, as any other asset, would probably be hit hard in the wealth destruction process but it was last used to peg money supply before 1971 (i.e. the gold standard).

I assume people would speculate on a gold standard 2.0.

Plus, gold is negatively correlated with real interest rates. As we keep on pushing real interest rate down to kick the can down the road, gold can be a decently performing tail hedge before the system actually implodes.

If you select the cheapest ETFs representing the above macro asset classes, the annual fees for this portfolio amount to a whopping 0.24% per year.

The ludicrous amount of fees charged by ‘‘financial consultants’’ out there is almost criminal, in my opinion. We’re talking 7-10x the 0.24% mentioned above. Please remember these 2%+ annual fees compound against you over time and are very often not backed by any tangible added value especially in terms of overperformance to a very straightforward portfolio like the one you see above.

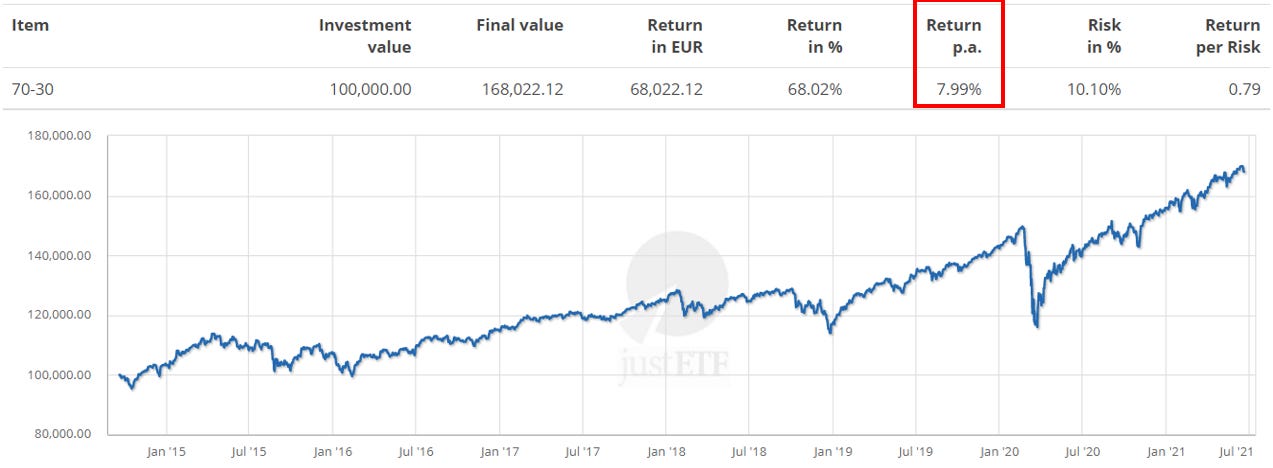

This simple 70-20-10 portfolio generated 8% nominal return on average over the last 7 years. This is 7% per year in inflation adjusted terms.

I hope you enjoyed the first edition of the Portfolio Approach!

I was wondering if you guys have any particular topic you’d like me to cover on Thursday in the next TMC edition? Feel free to answer in the comments. I will have a look and cover the topic which was mentioned the most!

If you like The Macro Compass, please help me grow by sharing this article or the link to the newsletter homepage in your network or on social media. Takes you 1 minute and it would help me a lot! Thanks and see you soon on TMC!

Hi!! In this article (in spanish) they justify that is better to have equities not hedged and bonds hedged. Why do you use this strategy?

Thanks

https://blog.indexacapital.com/2017/09/11/fondos-con-sin-cobertura-divisa/

Ciao Alfonso,

Any thoughts on portfolio rebalancing and frequency? Do you trim your tactical portfolio and transfer your profits into your long-term strategic asset allocation portfolio? If so, aren't you jeopardizing the beauties of compounding if you happened to be successful trading 10% of your capital? If not, how would you handle the eventual over/underexposure?

Grazie!