Run It Hot, Yet Again

I am back with a healthy dose of macro analysis for you

Hi nice people, this is Alf.

Sorry I disappeared from Substack for a good while but markets are crazy, the fund is growing nicely and it’s a huge amount of work.

But no worries - I am back with a healthy dose of macro analysis for you.

As an exception to the norm and to gain back brownie points with you guys, I am sharing the latest research piece reserved to the investors and The Macro Compass subscribers.

Here it goes!

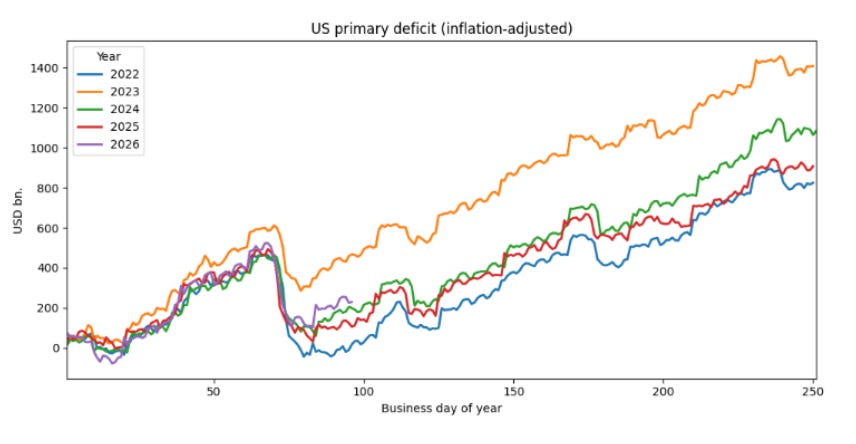

Forward-looking indicators suggest the US nominal growth cycle is picking up pace again. The inflation-adjusted primary US fiscal spending is higher than in 2024-2025 at this point of the year:

Global real-economy money printing is also growing at a strong pace, similar to 2025.

As a reminder, inflationary money is printed by governments (deficits) and via credit creation (banks, shadow banks etc). Concerted G20 fiscal deficits and the debt-funded AI capex cycle are the main contributors to the strong pace of global money printing in 2026:

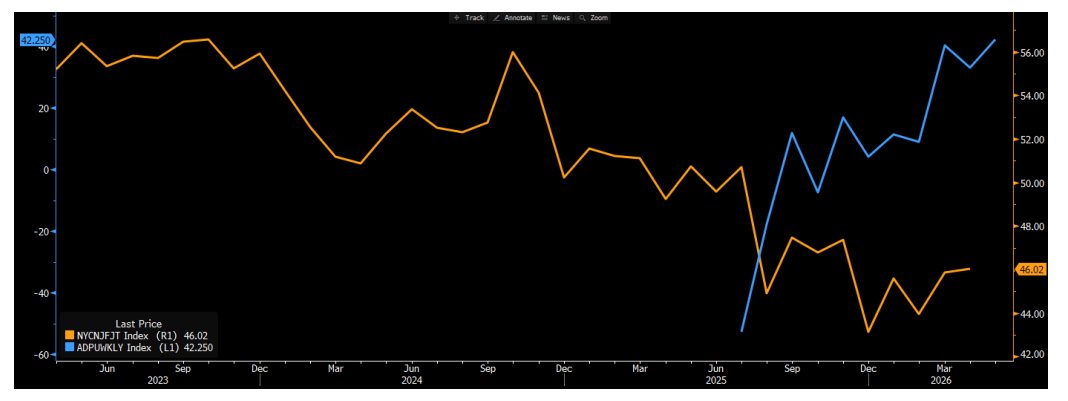

Leading indicators also suggest the US labor market has found a bottom.

The NY Fed probability of finding a job in the next 3 months (orange) has stabilized and the weekly ADP job creation series (blue) has moved from -50k in June 2025 to +42k today.

As a reminder, with the US labor force growth (e.g. supply side of labor market) estimated to be close to zero it doesn’t take much demand for labor to kickstart a virtuous cycle in the US job market:

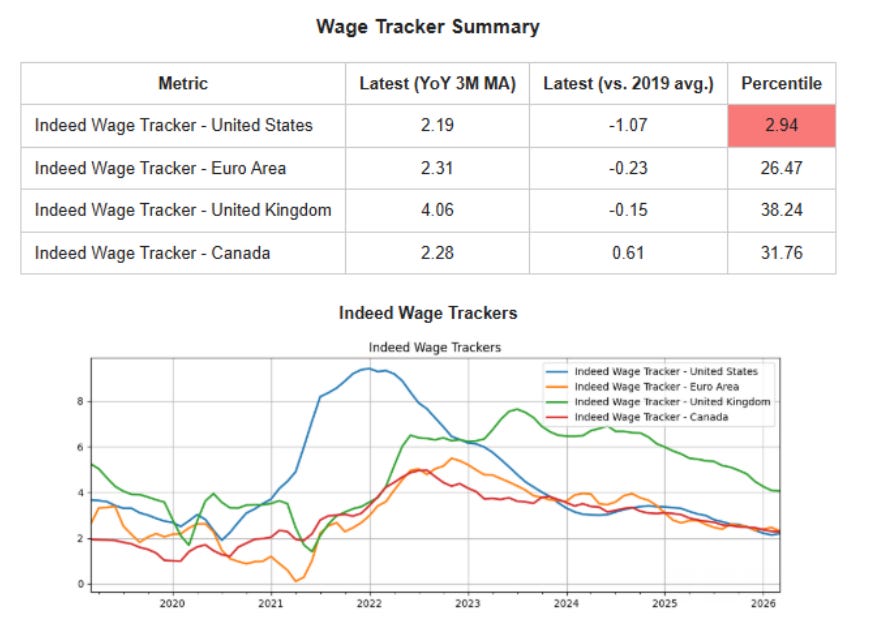

A virtuous cycle in the US job market won’t necessarily mean runaway inflation, at least in the short term. While a tighter job market will heat up wages, the starting point for US wage growth is very modest:

The Fed’s dual mandate of a) not letting the job market fall apart and b) core inflation below 3% (yes, sorry, not going to pretend the Fed has a 2% target anymore) would now call for a different reaction function.

‘’Would’’ is the key word here.

The December Fed meeting is now priced at a robust probability the Fed will hike. Yet to hike rates, the FOMC needs a majority of voters to lean in.

There are 12 voters, and a 6-6 situation gives the FOMC Chair the power to break the tie.

And the new FOMC Chair was recently talking about shrinking the balance sheet as a cover to cut rates and moving the inflation benchmark from core PCE to trimmed mean PCE (you guessed it, trimmed mean PCE is lower than core PCE)…it’s safe to say Warsh would rather eat his hat than raise rates.

In other words, you’d need 7 FOMC members voting for a hike to actually get a hike.

Even assuming the 3 dissenters against the dovish language in May would outright vote for a hike, and Barr would join them (quite some assumptions already!), you need 4 more votes for a hike coming out of this group: Warsh, Williams, Powell, Cook, Bowman, Waller, Paulson, Jefferson.

Yes, the BoE-zation of the FOMC is upon us. But I don’t think the FOMC will have a majority ready to hike any time soon.

Now, let’s assume my analysis holds. We would then find ourselves in the following situation:

US money printing is accelerating, and global money printing remains strong;

Nominal growth is likely to pick up;

The US labor market seems to have found a bottom, and might accelerate soon;

On the margin, this would add to inflationary pressures (but no runaway inflation dynamics yet);

The standard reaction function from the Fed should be to move to hikes (and the market asking for it);

The Fed is unlikely to have a majority actually voting for hikes any time soon;

So the title of the movie might be: Run It Hot, Yet Again

In that macro setup, my 40-year backtest shows the best trades to own are:

High-beta equities (small cap, EM, value tilt)

High-beta commodities (silver, copper, but also gold)

Long cyclical and high-yielding FX, short defensive tilt FX (e.g. ZARJPY)

Curve steepeners, short long bonds

I was recently in London meeting 3 large macro pod shops, and when presenting this thesis the biggest pushback or complete lack of interest sits with a) gold b) small cap, value, EM equities.

And that’s either a function of the AI dominance in equities recently or the ‘’it’s going nowhere’’ factor in precious metals such as gold and silver.

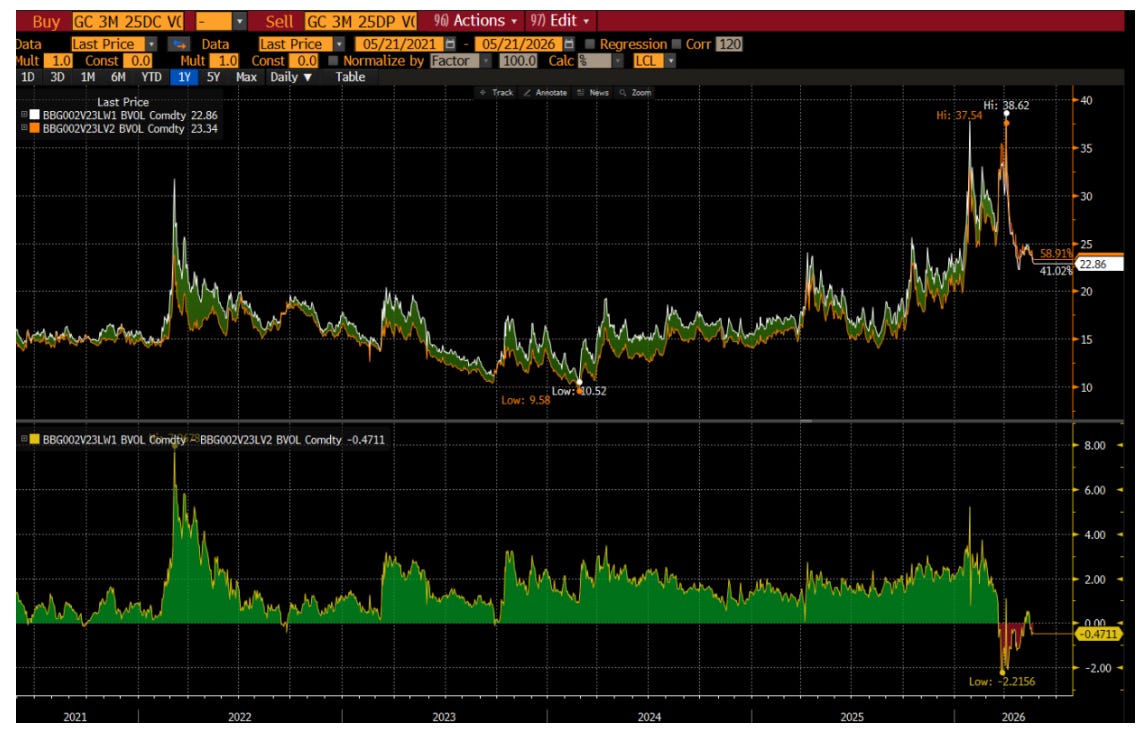

Option market positioning shows the same lack of interest towards gold upside. For the first time in many many years, 25-delta gold calls are trading at a discount to 25-delta gold puts. Investors are more interested in protecting against another drop in gold rather than buying gold upside:

Yes, I know: Hormuz. All the above is irrelevant if you think we escalate the war or there is no fix for months.

But if we unlock energy flows, we will Run It Hot. And the market is not fully prepared for it.

Thanks for reading!

To be in touch with me: alf@palinurocapital.com

I am so glad that I stopped to read it. Thank you!

Hallo