A Scary Bond Market

Term Premium Is Back - So Are The Bond Vigilantes?

Good morning and welcome back to The Macro Compass. This is Alf writing.

It’s almost been 3 years together now - and I loved every little bit of it.

I treasure each and every supportive comment you threw at me, and vividly remember hitting 100,000 subscribers and jumping out of joy. We are now 150,000+. It’s crazy.

But.

As I run two businesses now (my hedge fund Palinuro Capital and The Macro Compass), I need to focus on my customers even more.

So today I am asking you to become one.

Here is why:

A) You will read my macro insights multiple times per week

B) If you are quick, you get 40% OFF. Locked in forever.

C) This could be it. Next year we might close to new subscriptions.

Yes, you read it correctly.

As we are getting a large influx of institutional demand, next year we might be closing subscriptions at retail-friendly prices.

This is why today I am telling you: go for it.

The first 50 TMC readers who will use the code BLACKFRIDAY for our All-Round tier (multiple research pieces per week) will get 40% OFF forever.

You’ll end up paying only EUR 749/year.

That’s ~60 bucks a month to read my macro insights almost every day.

The offer is valid only for 3 days.

Use the link below. Be amongst the 50 who get in:

Now, to the piece.

The Bond Market is saying “This Time is Different”.

The Term Premium is on the rise, and it now sits close to the highest level for the last 10 years.

But What is Term Premium?

An investor looking to get fixed income exposure can do that via buying 3-month T-Bills and rolling them each time they mature for the next 10 years.

Alternatively, it can decide to purchase 10-year Treasuries today.

What's the difference?

Interest rate risk!

Buying a 10-year bond today rather than rolling T-Bills for the next 10 years exposes investors to risks – term premium compensates for this risk.

The lower the uncertainty about growth and inflation down the road, the lower the term premium and vice versa.

Uncertainty is the key word here!

The higher the uncertainty about future growth and inflation, the higher the term premium.

The left chart below shows how term premium (y-axis) increases with a higher dispersion of forecast (read: uncertainty) for inflation (x-axis):

Today the estimates of the US Term Premium have moved higher and they are now testing the upper side of recent ranges: in other words, there is some more uncertainty being priced in about the path ahead for growth and inflation.

Investors are less confident about a future of predictably contained inflation and growth, and they expect some more volatility and uncertainty down the road.

As we approach US elections, bond markets are telling us - yes, “this time is different”.

Persistent fiscal deficits regardless of who wins US elections can lead to more volatile inflation backdrops, and to more boom/bust cycles.

But as Term Premium is on the rise, should we fear the return of Bond Vigilantes?

Not so fast.

This week, Bond Vigilantes are in action in the UK: the fiscal budget unveiled by the new UK government has been assessed as ‘‘too loose’’, and therefore investors are going after all UK assets - they are selling GBP, selling UK bonds, and even stocks.

Bond Vigilantes are truly in action when they initiate a sell-off in bond markets to impart discipline to policymakers, and they hence generate a spill-over effect to the currency and potentially stock markets too.

But the US is not the UK.

Over the last 40 years, Bond Vigilantes have NEVER been in action in the US:

Over the last 40 years, we never really had investors puking on US assets - true Vigilantes are in action when both bond yields go up, and the USD goes down.

As you can see from the chart, that quadrant is basically empty.

We are instead experiencing people pushing US yields higher and the USD getting stronger. The bond market is hence sending a different message.

''Trump's policies will be stimulative for nominal growth, and the US will grow faster than other countries''.

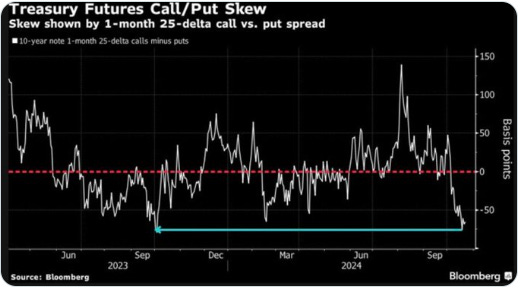

Additionally, investors are hedging for a scenario in which rates move up fast via options. This is evident in the so-called ''skew'':

This means investors are willing to pay more for bond puts than for bond calls for the next month.

This is unusual: investors normally pay more for ''insurance premium'' (bond calls) than for puts, so this is related to election hedging.

There are no ''Bond Vigilantes'' in action here.

Instead, the bond market is preparing for a Trump victory and for policies that will be stimulative for growth and inflation.

Yet, history shows us this.

Elections are a powerful short-term volatility event.

But macroeconomic cycles tend to prevail over time.

Trump was the President in 2019 as well, but as the global macroeconomic cycle was weak 10-year Treasury yields traded as low as 2%.

If Trump secures a sweep, I expect the bond sell-off to accelerate.

Your mother and your dog will tell you to sell bonds at 4.50% yields.

That’s when you should consider buying them instead.

And don’t forget: today you should go for it.

The first 50 TMC readers who will use the code BLACKFRIDAY for our All-Round tier (multiple research pieces per week) will get 40% OFF forever.

You’ll end up paying only EUR 749/year.

That’s ~60 bucks a month to read my macro insights almost every day.

The offer is valid only for 3 days.

Use the link below. Be amongst the 50 who get in:

Enjoy your weekend,

Alf

Why would you be trying to sign up new subscribers yet inform us that there are limited numbers? Very strange

Great info — as always — thanks Alf 🙏