The bond market is talking, and you'd better pay attention

TMC #9! The private sector is over-leveraged and structural GDP growth is poor: we can't afford higher rates. The bond market knows it, and it's trying to talk to you: would you listen?

10’ reading time (hopefully well spent)

Welcome back to The Macro Compass!

The publication is now 1 month old (I should say 1 month young) and we’re up to almost 2k subscribers. This is outstanding by any metrics, you guys are the best!

As always, I’d love if you could keep helping me by sharing the newsletter in your (social or professional) network.

The more, the merrier!

The US labor market - a pulse check

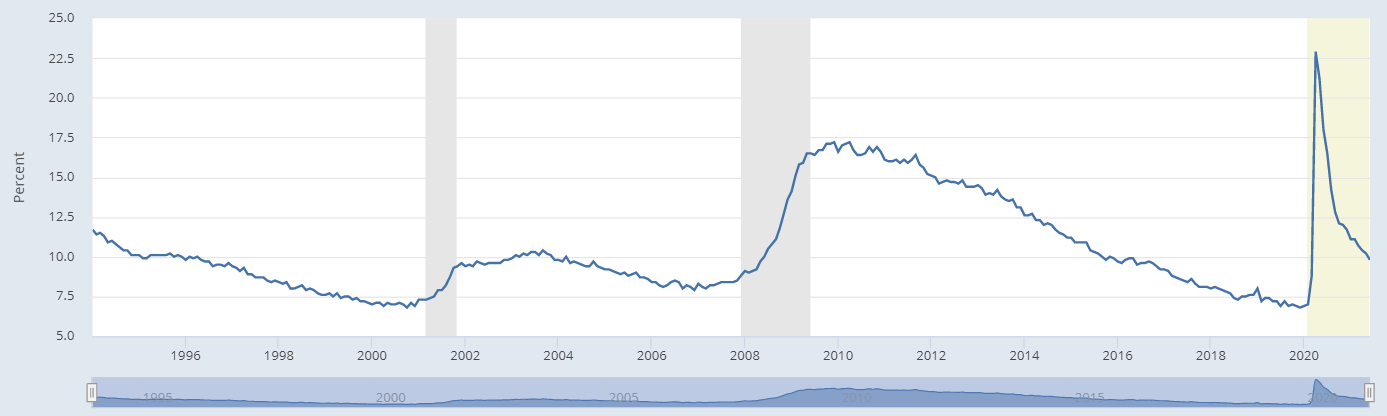

Last week we had the US June labor data and I think the report came in pretty decent. Most headlines focused on NFP at 800k with upward revision to prior figure, stable wage growth and slightly higher U3 unemployment rate.

As discussed in a previous post though, I think you should rather pay more attention at my preferred indicator for broad labor market slack U6 which ticked <10% for the first time since the pandemic.

You can consider the US labor market to be relatively tight once U6 drops to 7% and participation rate inches back towards 63%. What’s that?

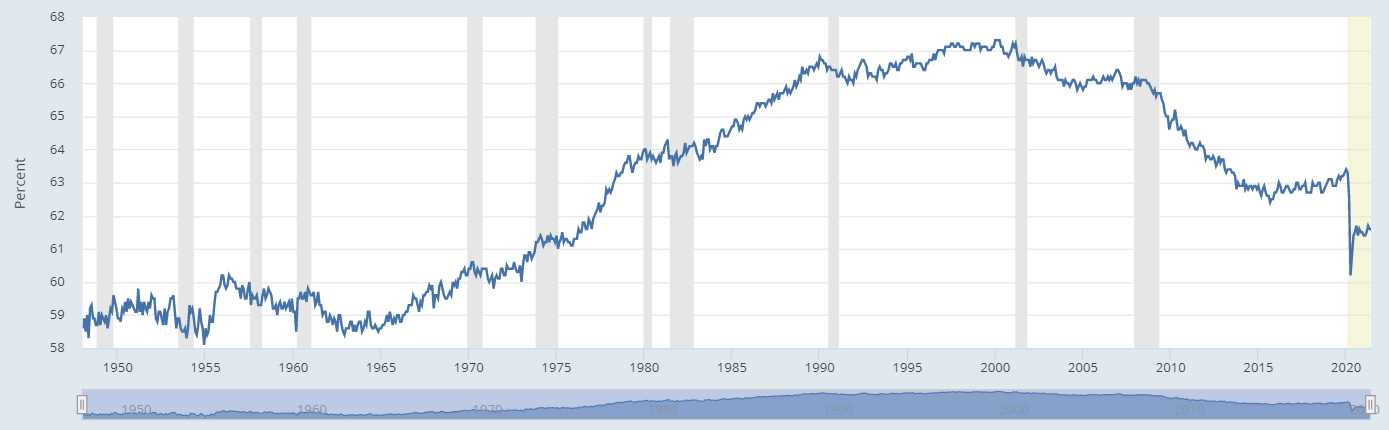

Participation rate measures the % of the US adult population which makes it into the labor force statistics. It now stands at 61.6%.

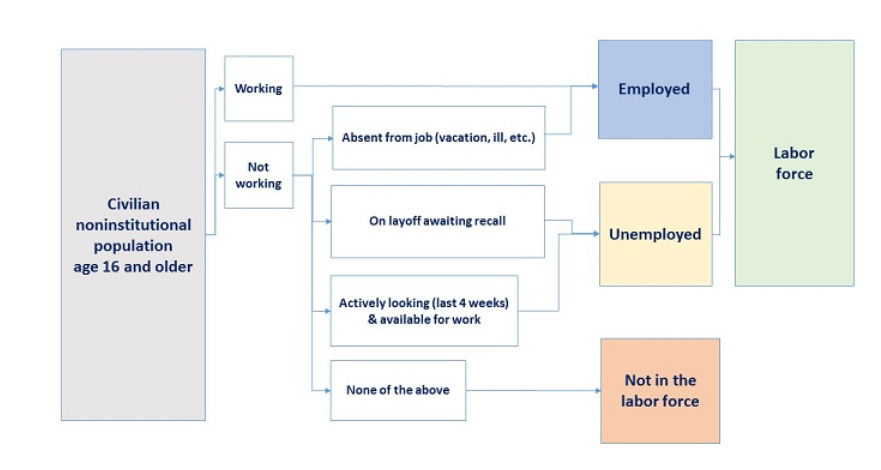

The diagram below might help you understand who makes into the labor force according to the statistics. Basically you have to be employed or otherwise unemployed but actively looking and willing to work.

Effectively, the pandemic not only got people fired or back into non-voluntary part-time, temporary jobs (U3 and U6 unemployment rate up) but also kicked a good 2% of the US working force population out of the labor force at all.

That means these guys haven’t looked for a job at all in the last 12 months and they are not interested in one at all.

The size of the labor force matters a great deal for long-term potential growth while the amount of discouraged, marginally attached workers describes the cyclical labor market slack very well.

Participation rate and U6 unemployment rate represent great indicators. Make sure you follow them both rather than only focusing on the NFP headlines.

As government stimulus programs are rolled off from July onwards and the Fed reaction function has moved towards data dependency rather than AIT commitment, the next US labor reports will become structurally more important. Watch out!

The good old bond market says these are not the ‘70s: would you please listen?

Commentators: ‘‘Inflation at 4%!’’

Bond market: ‘‘Yes, we know; 1y US inflation swap is priced at 3.6% already…’’

Commentators: ‘‘Credit spreads are tight despite horrible fundamentals!’’

Bond market: ‘‘Yes, we know; but the Central Banks are scooping up all of the net supply and the incentive scheme is there for us to chase all carry trades’’

Commentators: ‘‘The Fed is definitely behind the curve, runaway inflation is here! This is like the ‘70s, it’s a regime change!’’

Bond market:

I had a chat with Mr. Bond Market over the weekend. He’s a bit tired of being right for 40 years about the fact there is no regime change, but he asked me to point out at one very important element people always forget: the private sector.

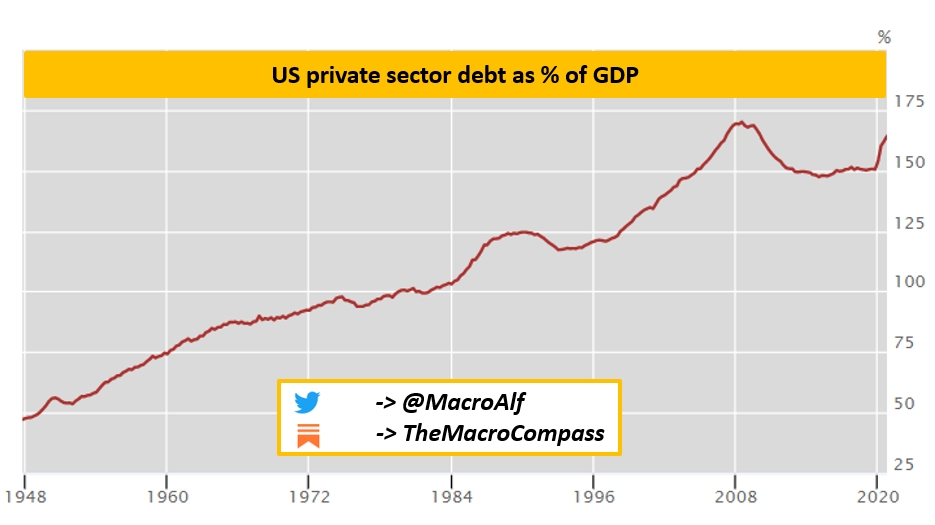

Firms and households are over-leveraged up to their nose.

Their appetite for additional credit is extremely low and without credit demand there is no sustainable push to aggregate demand aside from structural growth.

Look at how private sector as % of GDP went up from 75% in 1960 to almost 100% in 1975. Now compare that to the flat-lining you see between 2010 and 2020.

The pandemic caused an increase of private debt / GDP to 165%, just shy of the GFC highs at 173%. Please notice the private sector is a currency user, not a currency issuer like the government. They need cash flows to service their debt.

An over-leveraged private sector composed of an ageing population and a large portion of zombie companies facing a structural lack of productive investments outlet is NOT going to borrow more. The private sector wants to de-leverage.

Now, add to that the latest range of estimates for US real structural GDP growth which stands at 0-0.25%.

So, weak structural growth and poor appetite for credit = no runaway aggregate demand = …runaway inflation?! Really?

Inflation is and will remain >2% for few quarters as supply bottlenecks during a global pandemic are basically there by design and it takes some time to solve them - but they will be largely resolved.

Inflation is also temporarily high because there was a HUGE, temporary boost to aggregate demand in the form of credit creation via deficits and government sponsored bank lending.

But banks are not lending anymore already, as the RoE on loan books is horrible due to low loan yields and tight capital requirement. Plus the creditworthiness of the borrowers out there is not that great.

So you’re putting all your chips on government stimulus to continue at an ever increasing pace every single year.

Please realize that runaway inflation needs the government alone to create credit every year, and more of that every single year. Not only the direction of travel must be net deficits forever, but at an accelerating pace.

Also, please realize you are implying the private sector will spend that money rather than pay back debt or save it. >50% of 2020-2021 stimulus was used for the latter…

In the ‘70s, you had potential growth at 3-4%, private sector appetite for credit (as shown above), strong bargaining power due to labor unions and a labor intensive industrial age and no scalable, deflationary tech forces.

How can you even compare the ‘70s to today?

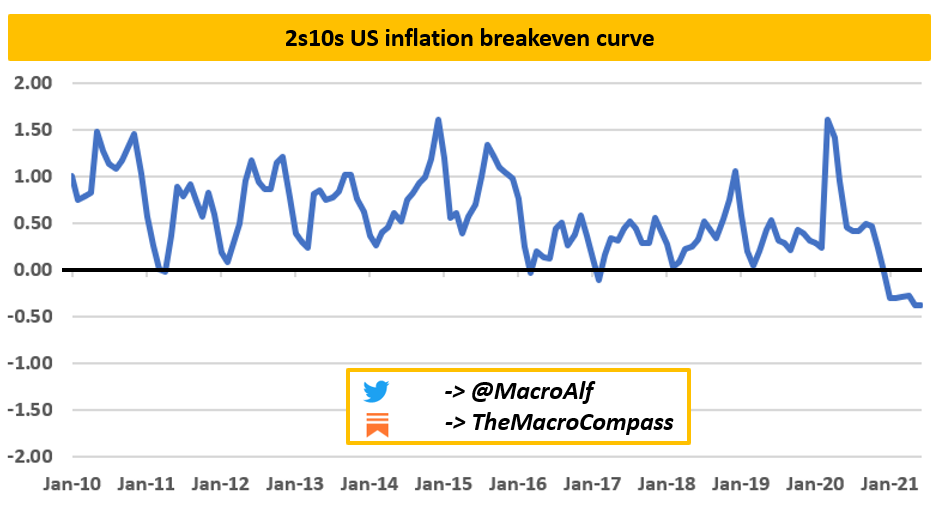

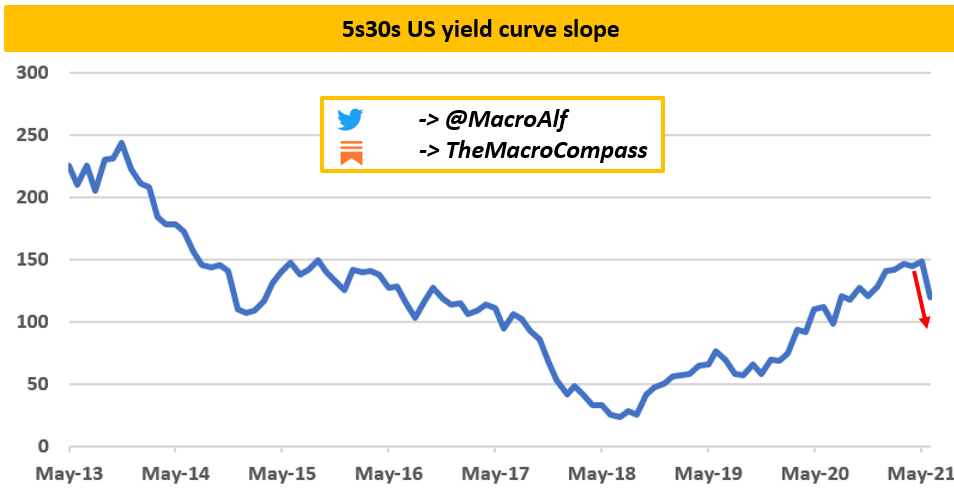

Here is what the bond market thinks of the ‘‘regime change’’ narrative encompassing runaway inflation and higher rates, in two charts:

The spread between 10y and 2y inflation breakeven rate is negative.

The bond market prices 2y inflation at 2.7% and 10y inflation at 2.3%, which basically means it strongly disagrees with the runaway inflation narrative medium-term.

The US yield curve slope between 5y and 30y started compressing aggressively as soon as the Fed signaled their very first intention to (maybe!) remove some policy accommodation. The bond market knows potential growth is poor and the economy is way over-leveraged, and hence if short-end yields are repriced up (Fed tightening) then long-term yields have to drop to price in even slower nominal growth.

Now, the bond market has been right about the structural deflationary forces for about…40 years and counting.

To wrap it up

Listen to Mr. Bond Market. He’s often right, and he has good reasons for it.

The next decade has nothing to do with the ‘70s, and a lot to do with an over-leveraged and poor structural growth economy.

What also should you know?

Last week, I recorded an interview with Real Vision which is going to be published on Wednesday. Follow me on Twitter, this way you won’t miss it!

I closed my short Eurostoxx trade on Friday at around the same level I entered it (4.070). It did absolutely nothing for few weeks and it seems not to be the best risk/reward expression of the transition towards the next Quadrant. Let’s take the chips off the table and re-assess.

Also, if you are looking for high-quality macro content from an experienced guy who traded proper risk for banks and has still skin in the game, have a look at Kevin Muir’s The Macro Tourist newsletter.

If you like this article, feel free to share it with your (social) network!

Reminder: everything you hear or read from me on Substack, podcasts, Twitter, Linkedin etc is solely my own opinion and it does not represent my employer’s views or opinions. I speak and write on behalf of myself, Alfonso, macro enthusiast and private investor.

See you at the next update!

Hi Alf,

Was trying to check the 2 year breakeven rate as of today. Cannot find it. Any idea where to look?

Since TIPS are issued starting from 5 years, FRED only has break even rates for 5, 7, 10 and 30 y.

Hi. Today i re-read this article and have a comment:

I do not completely agree with the argument that debt repayment only narrows the money supply and does not promote inflation. Yes, by the time debt is paid, the money supply has shrunk.

During crisis, Creditors found themselves own a lot of bad, or unperformed loan.

However, when those loan on asset side of Creditor balance sheet are paid backwith stimulus money from Debtors (essentially the Government - Public sector - uses its own debt to absorb the risk from the private sector - essentially a wealth redistribution process) then Creditors will change their view about risk - Because now their balance sheet is healthier than before and they can lower lending standards, thus the money supply could increase again.