‘‘The FOMC is not actively considering 75 bps hikes’’

Jerome Powell, May 4th 2022 Fed Meeting

How do you assess whether the outcome of a Central Bank meeting was hawkish or dovish? Simple: you look at the delivered outcome against the probability distribution which was priced in before the meeting.

It’s not an absolute but a relative assessment.

Yesterday, the Fed delivered a 50 bps rate hike and a balance sheet run-off schedule which closely met expectations but the press conference turned to surprise expectations on the dovish side - and it was a mistaken attempt at sounding dovish, in my opinion.

In this brief article, we will:

Analyze the Fed decisions and the main highlights of the press conference

Look at market pricing across asset classes pre and post meeting, and assess what happened

Discuss what this Fed meeting means for your short and medium-term portfolio allocation

Without further ado, let’s jump right in!

I am Damn Serious about Inflation, Or Maybe Shall we say ‘‘Serious-ish’’?

Before we jump in, I want to share with you guys a lesson I learnt from my mentor.

’’Never proxy-trade; always trade the closest instrument to your underlying macro assumption as correlations can easily break!’’.

I’ve noticed you are often looking for easy, direct ways to trade your projections on inflation or the chances of a recession but it might be you don’t have access to complex derivatives and hence end up being forced with imperfect proxy trades.

I recently came across Kalshi and they provide a great solution for that problem: they allow you to directly trade probabilistic economic and market outcomes without the hassle of complex derivatives product or leverage!

For instance, you can buy "Yes" or "No" shares on markets such as "Will April inflation be higher than 0.4% MoM?".

Pretty cool company, check them out!

Now, back to it.

Yesterday the Fed proceeded with the first 50 bps interest rate hike since more than 20 years.

Moreover, the Fed announced a time schedule and a pace for their balance sheet runoff (QT): the Fed balance sheet will drop by more than USD 500 billion in 2022 and if the pace is kept constant, by an additional USD 1.1 trillion in 2023 too.

This decision package roughly met expectations, but the proper fun was in the press conference.

The presser started with a strong and concise message to Americans: we understand inflation is squeezing you, but we have your back. We’ll get this under control asap.

We are serious about inflation!

Powell then proceeded to paint a picture of how strong is the American economy and how tight is the US labor market: several times, he referred to the ratio between the big amount of job openings and the relatively small amount of unemployed people.

Here is the chart the Fed is looking at:

One note from my side is that while cyclically the labor market is indeed very tight, using this ratio ignores the fact that a large number (around 2 million) of the US workforce seems to have just left for good.

This makes the supply of available labor optically very tight, but a structurally shrinking participation rate doesn’t bode well at all for the long-term economic growth of a country.

Anyway, we had already heard this song from the Fed: the US economy is super strong and can take a proper amount of monetary policy tightening without much issues.

Now, shall we talk about how much that is and hence the forward guidance?

Here is where we had the two dovish surprises of the press conference, if you ask me.

1. ‘‘The committee is not actively considering 75bps rate hikes at this stage’’

We are watching fixed income markets trying to test the Fed’s resolve since the beginning of 2022 by pricing incrementally higher December 2022 implied Fed Funds rates and higher terminal rates for the Fed hiking cycle.

This was the probability distribution for the Fed meeting in June pre and post press conference:

The probability of a 75bps rate hike (orange bar) moved down, although markets are still trying to push the Fed in that direction.

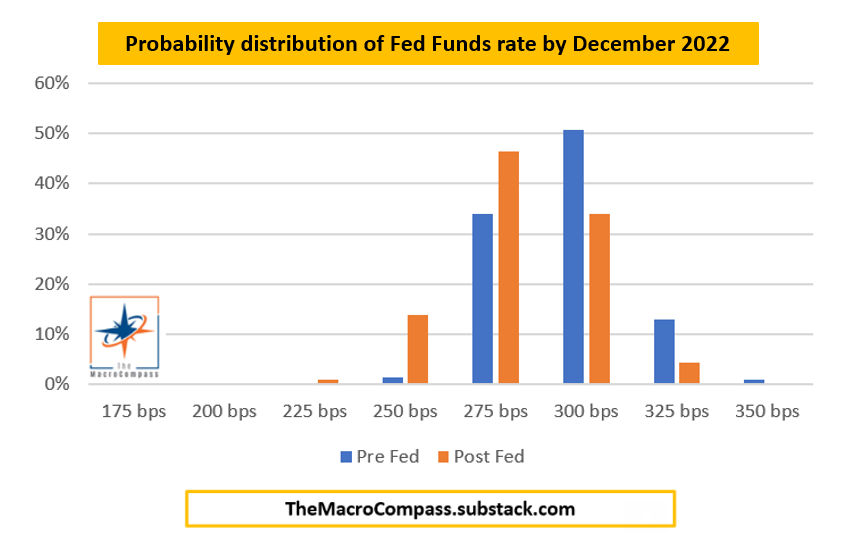

And this was the probability distribution for where Fed Funds are going to be in December pre and post press conference:

As you can see, the distribution moved to become centered around a Fed Fund rate at 2.75% by December (from 3% before) and the right tail became much thinner as the probability of Fed Funds rate above 3% almost disappeared.

By trying to truncate the right tail of the distribution, Powell attempted at removing some of the hawkish uncertainty in fixed income markets.

This lowered implied volatility and encouraged investors to reload on their risk assets exposures: indeed, equities staged a strong rally while credit spreads tightened and the US Dollar depreciated against most other currencies.

But wait a second: stronger equities, tighter credit spreads, weaker US Dollar…this basically means looser financial conditions?! We thought the Fed was all after tighter financial conditions here!

2. ‘‘Assuming that economic and financial conditions evolve in line with expectations, there is a broad sense on the Committee that additional 50 basis point increases should be on the table at the next couple of meetings’’.

After truncating the hawkish right tail (75 bps hikes), Powell then moved on to validate the base case market pricing of multiple upcoming 50 bps hikes but he stressed out ‘‘assuming financial conditions evolve in line with expectations’’.

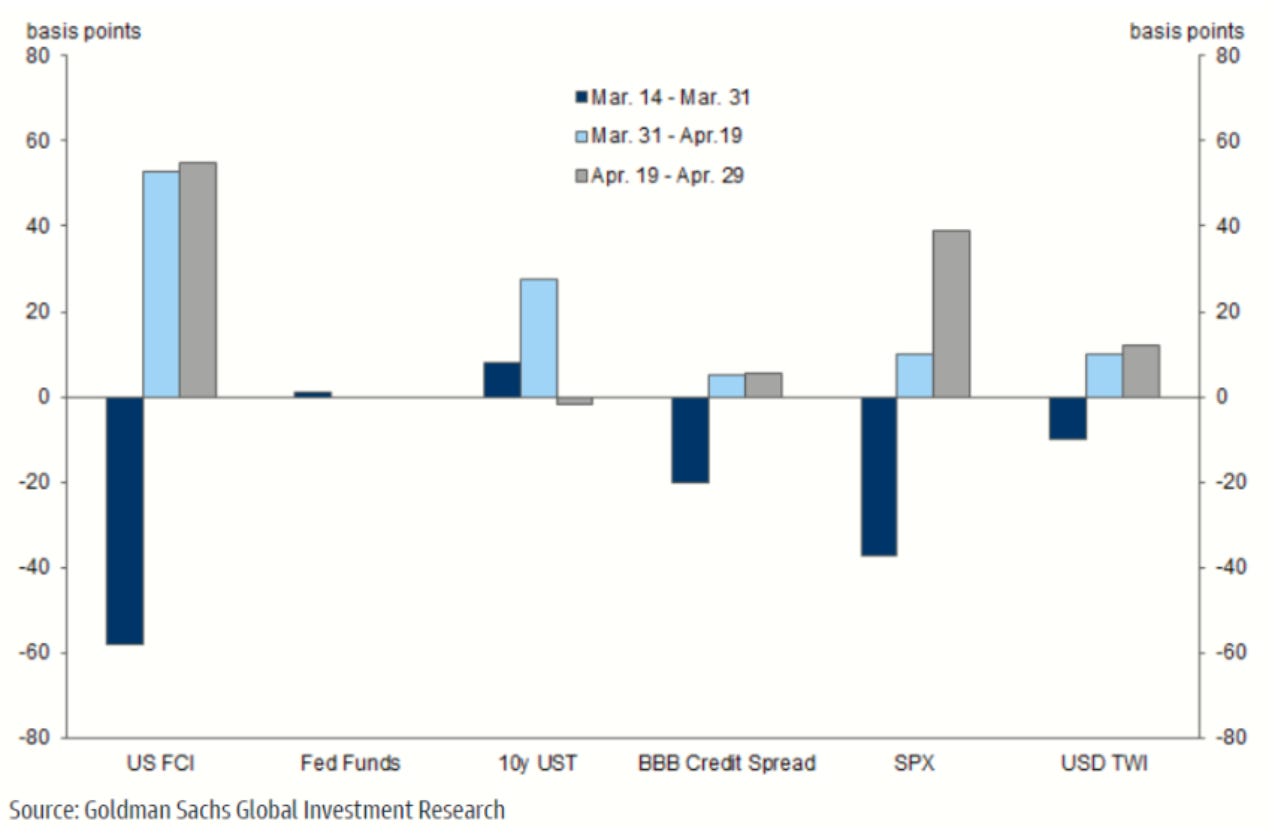

For reference, here is how the Goldman Sachs Financial Condition Index components moved from the 2nd half of March through the end of April:

April (grey and light blue bars) saw a sharp tightening in financial conditions mostly due to weaker equities and a strong trade-weighted US dollar.

Yesterday, Powell proceeded to first cut the hawkish right tail of the Fed Funds rates distribution and then told us the current bond market pricing is acceptable but only if financial conditions evolve ‘‘in line with expectations’’: it sounds to me as this was an attempt at sounding dovish and slow the pace of deterioration in risk sentiment.

Now, why do I believe this was a mistaken attempt?

Basically, markets will keep forcing Powell to choose between a gentle tightening of financial conditions and getting inflation (and expectations) firmly under control.

The more he tries to achieve both, the more he’ll let markets be in charge: if he winks at risk assets like yesterday, he gets a sharp loosening of financial conditions which goes against his very objective of slowing down demand and anchoring inflation expectations.

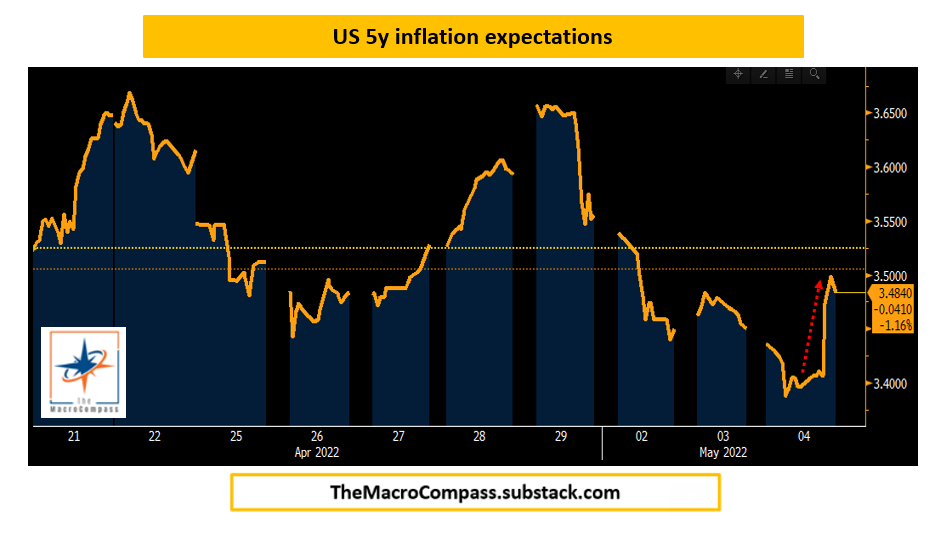

And indeed, 5y US inflation swaps went sharply up after yesterday’s FOMC: not what the Fed is hoping for.

In short, I believe Powell mistakenly attempted at sounding dovish yesterday and risked further credibility loss in his inflation fight - he can’t afford that to happen, and markets will keep on reminding him!

So, What About Your Portfolio Allocation?

While the Powell’s mistaken attempt might force a short-term risk asset rally similar to the one witnessed in the second half of March, medium-term my stance remains that risk assets can sustainably rally only if:

a) Things get much, much worse first.

This means financial conditions drop to a point where companies lose access to credit markets, or the functioning of the Treasury or repo markets are seriously impaired, or equity markets drop to a point where the labor market starts being affected via second round effects.

At that point, the Fed will need to reconsider things and ease financial conditions.

b) Inflation slows down faster than priced in forwards and expected by the Fed.

Inflation peaking is not enough: as often, it’s all about moves relative to expectations.

In order to allow the Fed to take the foot off the gas pedal, PCE needs to slow down even faster than their expectations (roughly 3% YoY PCE by year-end).

If that happens, they can credibly step back and as bond markets sustainably reprice their hawkish expectations down, risk assets can rally.

For the time being, we comfortably sit in the Quadrant 4 of our Macro Compass: the credit impulse has slowed dramatically and the monetary policy stance has sharply become tighter with a fast repricing up in real yields - in some cases to levels above equilibrium rates.

Hence a defensive asset allocation remains the soundest choice, in my opinion.

And this is (almost) it for today!

Last but not least, a new episode of The Macro Trading Floor podcast is out!

This week, Andreas Steno and I interviewed Simplify’s Chief Strategist and Portfolio Manager Mike Green and asked him to unpack her thesis and to deliver an actionable investment idea for our listeners - it was quite an interesting one, have fun!

Links here: Apple, Spotify, Google, YouTube.

Finally, stay tuned as I will be releasing my long-only macro ETF portfolio over one of the next articles here on The Macro Compass!

Thank you for making it all the way through :)

If you appreciate my efforts to deliver free financial education and macro insights, would you be so kind to click the like button and share this piece in your network?

It would really mean the world to me!

If you are interested in any kind of partnership, sponsorship, or in bespoke consulting services feel free to reach out at TheMacroCompass@gmail.com.

For more macro insights, you can also follow me on Twitter and Linkedin.

Feel free also to check out my new podcast The Macro Trading Floor - it’s available on all podcast apps!

See you soon here for another article of The Macro Compass, a community of more than 43.000+ worldwide investors and macro enthusiasts!

Share this post