Hey everybody, welcome back to The Macro Compass!

‘‘Long ago, Ben Graham taught me that price is what you pay but value is what you get. Whether we’re talking about socks or stocks, I like buying quality merchandise when it is marked down.’’

Warren Buffett

This is a special edition.

We have the pleasure to host a discussion with a great macro analyst: Lyn Alden!

I sat down with her for a fireside Q&A session on a stock market sector she believes is primed for outperformance.

Without further ado, let’s jump right in!

Alf: ‘‘Such a pleasure to have you here on The Macro Compass, Lyn! Let’s not waste time and dive right into it: what’s the equity sector you like here?’’

Lyn: ‘‘My pleasure, Alf! I am talking about the Healthcare sector.

Healthcare stocks tend to do better than the broad S&P 500 in risk-off environments and periods of slowing economic growth. The majority of economic indicators look much weaker for 2022 than they did for 2021.

This following chart shows the ratio of healthcare stocks to the broad S&P 500, and you can see that the spikes are generally associated with recessions and risk-off periods.

These spikes include the Savings and Loan crisis (early 1990s), the Asian Financial Crisis (1997-1998), the aftermath of the dotcom bubble (early 2000s), the aftermath of the subprime bubble (2009), the oil crash and global economic slowdown (2015/2016), the liquidity issues that resulted in the Powell Pivot (late 2018), and the COVID-19 crash (early 2020).

I wouldn’t be surprised to see another leg up for that ratio in the coming years, and quite possibly within 2022.’’

Alf: ‘‘So, from a cyclical macro perspective it seems you believe we are entering a cyclical economic slowdown and perhaps leaning risk-off here?’’

Lyn: ‘‘Yes: an economic slowdown is in the cards. Further fiscal stimulus has been on hold due to Senate gridlock, high energy prices are eating into consumer pockets, and the economy is coming down from somewhat of a sugar high. The flattening yield curve suggests future economic weakness, and so does the Atlanta Fed’s GDPNow indicator, which currently models 1.3% annualized real GDP growth for Q1 2022 based on a wide array of economic data points.

The purchasing managers’ index and various leading indicators continue to suggest economic deceleration is in store for 2022

Alf: ‘‘Alright, but the impulse to economic growth has started to slowdown in the second half of 2021 already: why have healthcare stocks struggled in that period, too?’’

Lyn: ‘‘For the second half of 2021, many healthcare stocks, especially pharmaceutical companies, were held down by the possibility of legislation that would control their prices. Democrats in the House of Representatives passed legislation to limit their price increases in line with inflation, and allow for more negotiation by Medicare. When it came time for inclusion in the Build Back Better bill, which had to get through a tightly-divided Senate if it was going to pass, the legislation was watered down. Even then, however, the entire Build Back Better bill stalled, and healthcare price reform remains in limbo.

With a divided US Senate, there doesn’t seem to be any major healthcare reform on the horizon that would disrupt healthcare stock profitability in a major way. Polling currently suggests that the government will be even more divided after the 2022 mid-term elections, which further pushes away the horizon for serious reform.

Meanwhile, healthcare stocks generally have attractive valuations. They’ve not been piled into by hedge funds or meme traders, and have generally been unloved in a risk-on environment while drug pricing reform added an extra layer of uncertainty.

Alf: ‘‘Fair points! Do you have a couple of names investors could look into?’’

Lyn: ‘‘Yes, two names within a sector that remains overall attractive.

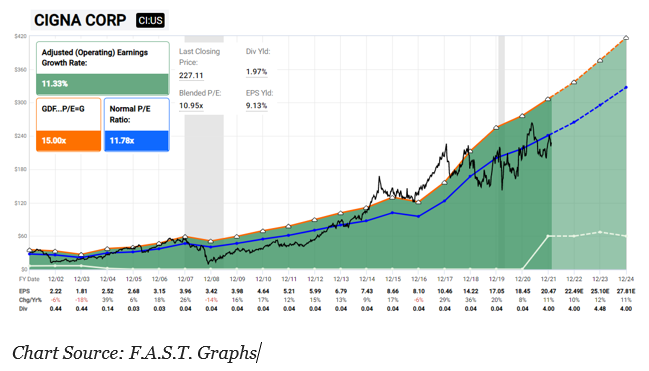

Cigna (CI), a health insurer and pharmaceutical benefits manager, is trading at under 11x earnings with solid growth. It initiated a dividend in early 2021, and then raised that dividend by 12% in early 2022. The credit rating is A- by S&P.

At a deeper value but with less growth is Bristol Myers Squibb (BMY). It trades at 9x earnings and has a dividend yield of over 3%. The company is reliant on a few blockbuster drugs, but due to its 2019 acquisition of Celgene, it also has a decent long-term pipeline of new drugs. The credit rating is A+ by S&P.

While I wouldn’t bet too big on any one stock, the sector seems attractive.

A diverse collection of healthcare stocks seems primed to outperform Treasuries over a 5-year view, with better yields and then some growth on top. Unlike many other areas of the stock market, there are no significant signs of overvaluation in the healthcare sector.

Since healthcare stocks trade away most of their cyclical risk in exchange for having more regulatory risk, but with regulatory risk held back for the moment, they are well-positioned for 2022 in my view.’’

Thanks to Lyn for this good piece and macro chat with us on The Macro Compass: in case you are not following her, you should do that on Twitter and subscribe to her newsletter here.

Lyn Alden is one of the most intelligent and well-grounded macro people out there, and she conveys complex macro topics in a very concise and clear way: a must follow!

I agree with Lyn’s 2022 cyclical macro slowdown thesis: the credit impulse has quickly faded away since early 2021, and Central Banks intend to tighten fast back to (at least) neutral interest rate levels while inflation expectations have likely topped.

This would continue pushing real yields and credit spreads up in an unfriendly way, and flatten yield curves all the way towards inversion.

In such an environment, risk assets tend to struggle and it’s best to find ‘‘healthy’’ sectors to invest in if you really want to keep your exposure to equities: low-beta, high-quality companies tend to outperform the broad market returns during these periods.

The healthcare sector (IYH for US, IXJ for global healthcare) reflects most of the features described above.

Last famous words.

If you enjoy my work, please consider clicking on the like button at the end of the piece and share the article.

It would cost you literally nothing, but it would really make my day!

Are you looking for any other kind of partnership or collaboration?

Are you an institutional investor who likes The Macro Compass and would be interested in a bespoke, pro-to-pro coverage?

For any inquiries, feel free to get in touch at TheMacroCompass@gmail.com.

If you want more macro insights, you can also follow me on Twitter and Linkedin.

See you soon here for another article of The Macro Compass, a community of 28.000+ worldwide investors and macro enthusiasts!

I will be off next week, hence the next piece will be released on March, 7th.

Stay tuned!

Share this post