Hi all, and welcome back on The Macro Compass.

In this timely piece we are going to cover the recent Bank of Japan meeting and its implications for markets.

Before we start, a kind reminder: if you find value in the timely macro analysis and portfolio strategy The Macro Compass provides, this (and much more) will very soon require a paid subscription.

Gates are closing in only 10 days: check out which subscription tier suits you the most and come join us - I’ll be waiting for you to come onboard!

Surprise, Surprise!

We all woke up to a major macro surprise: the Bank of Japan (BoJ) widened the allowed trading band for the 10-year Japanese government bonds (JGBs) by 25 bps - 10y JGBs can now trade between -50 bps and +50 bps.

While this doesn’t seem like a major change, it really is.

To understand why, we need to take a small step back.

For years, Japan implemented an aggressively dovish monetary policy stance.

Bank of Japan rates were effectively pinned at 0% for decades.

Large-scale QE was standard practice, and a few years ago the BoJ switched to Yield Curve Control (YCC).

This was necessary as relentless QE purchases had led the BoJ to own >50% of the Japanese government bond market, and buying more bonds would seriously alter the functioning of the market. For days, there were basically no trades happening in the JGB market.

So to keep 10-year yields low, the Bank of Japan moved from targeting a quantity of bonds to buy (QE) to a qualitative measure (YCC).

It was a successful move: the charts below show how predictable the BoJ monetary policy was - front-end rates stuck at 0% for decades, and 10y JGBs constantly trading in the prescribed +/- 25 bps yield range for 6+ years.

Until today.

But Alf, the BoJ didn’t raise rates and they widened the 10y JGB trading band by a mere 25 bps: how can such a ‘‘small’’ move have worldwide macro implications?

It does because global macro is a giant interconnected puzzle - bear with me.

Japan is a huge exporter of capital.

Since the '90s, Japanese investors are used to look abroad for opportunities to deploy their domestic excess savings.

For instance, as of July 2022 (left chart) Japanese investors are the largest holders of US Treasuries in the world - Japan accumulated over $1 trillion in USTs as it was a convenient way to recycle excess savings: yield differentials were positive, and often more than offsetting the cost of hedging USD/JPY risks.

The right chart below shows how convenient it was for Japanese investors to buy Treasuries and cover the FX risks. They would on average get a 100-150 bps additional return by purchasing USTs rather than simply buying Japanese government bonds.

The BoJ decision and the new direction of travel can significantly alter this flow of capital - one of the global macro impacts of today’s BoJ decision.

Said that, to really grasp the potential market implications and trade opportunities going forward we must answer two main questions.

#1: Why Now, And Will The BoJ Continue Along This Path?

The best macro investors are always keen to assess a crucial yet elusive variable: policymakers’ incentive schemes.

Here is my attempt at doing that for Japan.

Japan has a new Prime Minister (Kishida, who succeeded Abe) and in April 2023 BoJ Kuroda’s term will expire - hence, it will have a new Governor of the Bank of Japan too.

Abe and Kuroda worked together to try and pull Japan out of a deflationary spiral, and while it can be argued they didn’t succeed much so far Kuroda now has the chance to leave office with a ‘‘victory lap’’.

Core inflation in Japan could soon stabilize around 2%, and while the BoJ has basically nothing to do with it Mr. Kuroda is likely to seize the opportunity.

The cherry on the cake would be to lay the foundations for a new (more hawkish) monetary policy path his successor could follow.

And that’s my answer to the ‘‘why now’’ question.

Will Kuroda’s successor continue along this path?

I think so.

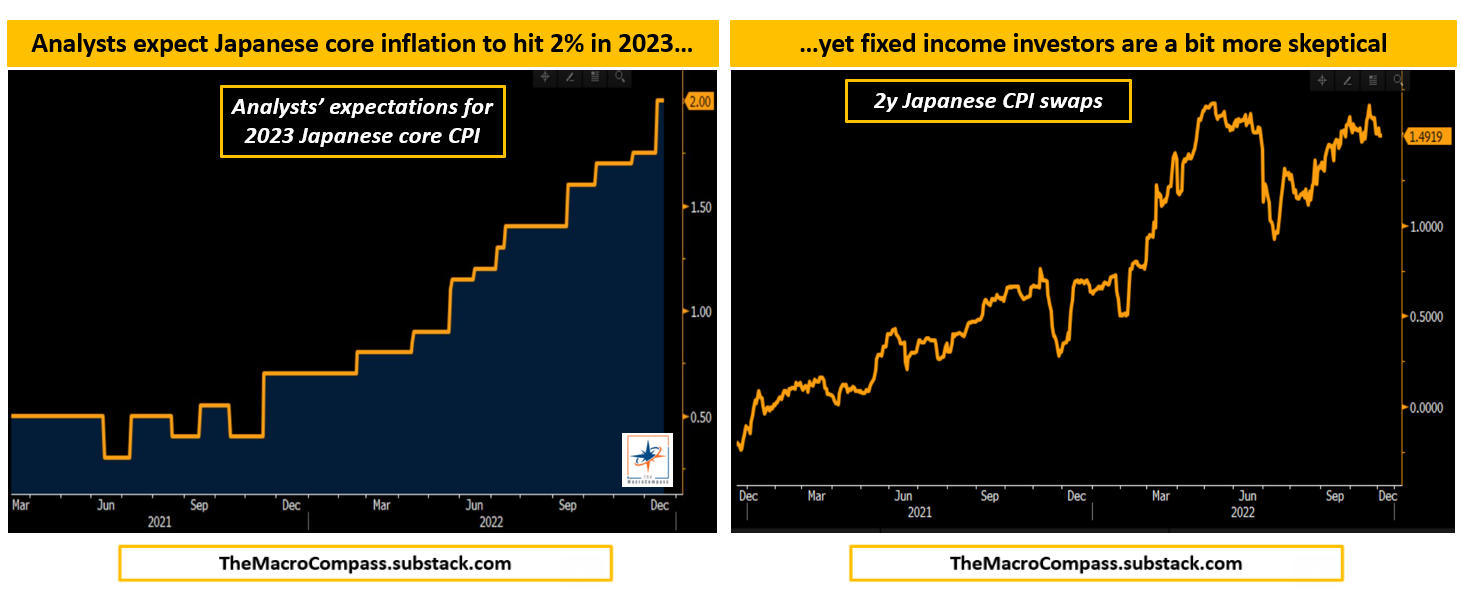

And that’s because core inflation is likely to keep trending towards 2% (left chart), and despite fixed income investors not being fully convinced (right chart) yet they are also expecting Japanese CPI to justify a more hawkish stance.

The ‘‘new sheriff in town’’ approach is relevant because it signals this is not a one-off move, but rather a sustained shift in the approach to monetary policy and inflation.

The second important question to grasp macro implications and potential trade ideas is: what are markets pricing in at this stage?

#2: What’s The Market Pricing In?

Tracking global market moves across their many dimensions and assigning the right relevance to each mover is very hard - but the Volatility Adjusted Market Dashboard (VAMD) will fix that for you.

You’ll literally be able to screen the entire global macro universe in a fully customizable way, identify the biggest vol-adjusted moves and draw analytical charts to test your macro ideas.

The VAMD is telling us that:

Despite the BoJ not raising deposit rates, markets are pricing in 30+ bps hikes in 2023 (1y1m OIS at +27 bps, spot in negative territory) and an additional 25 bps hikes in 2024 too;

The yield curve dramatically flattened in the 5s30s segment, indicating bond markets expect this sudden hawkish shift to weigh on the already poor long-term nominal growth prospects in Japan;

Bond volatility picked up aggressively across the board.

On top of that, USD/JPY dropped like a stone.

In other words, fixed income and FX markets are taking this seriously and extrapolating a hawkish BoJ reaction function well into 2023.

This is not to be treated like a one-off small move.

P.S. The VAMD is available for All-Round Investor subscribers.

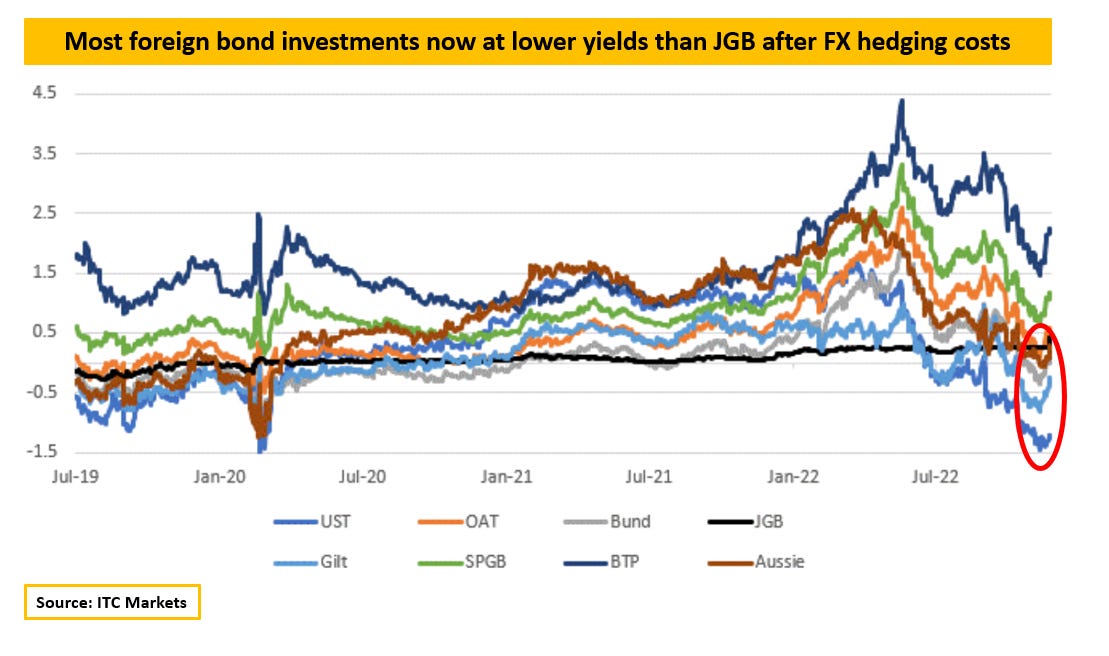

Another important macro implication is evident in the global fixed income market.

As said before, Japanese investors are heavily involved in foreign investments and in particular in purchasing highly-rated government bonds issued by the US, European countries, UK and Australia.

By affecting JGB yields and the JPY, the Bank of Japan largely impacted the financials of these gigantic cross-border capital flows in the bond market.

The chart below shows how after today Japanese investors won’t find any additional yield by purchasing foreign bonds vis-à-vis JGBs unless they buy Spanish or Italian bonds - which will be under pressure as the ECB tightens policy and embarks in QT.

Now that Japanese investors are getting positively rewarded to keep their cash at home during a global economic slowdown and periods of high macro uncertainty... ...they probably will choose to do that more.

That strengthens the Yen, and negatively affects foreign assets.

So, what are the implications for trades and portfolios?

Conclusions & Portfolio Implications

Another day in 2022, another tectonic shift by a globally important Central Bank: this time the Bank of Japan.

Given the policymakers’ incentive schemes, this isn’t likely to be a small one-off adjustment but a new monetary policy approach to inflation which involves a more hawkish BoJ stance with important global macro implications for asset classes.

I already liked the JPY, and on a medium-term basis I like it more now.

I expect a global recession in 2023, and the Yen tends to strengthen in such an environment as yield differentials compress and Japanese investors are incentivized to bring money home rather than seeking risks in that tough macro environment.

With the BoJ enhancing those incentive schemes via higher domestic rates, the Yen might appreciate even further.

Long JPY exposure can be achieved via FX account, or via $LJPY ETF for US investors or $EUJP for European investors.When it comes to bonds, the already dwindling support of Japanese investors for European and US bond markets will shrink further.

This in particular supports my short-term bearish thesis on European rates.Finally, as another Central Bank joins the ECB and the Fed in tightening policy and increasing risk-free rates this bodes negatively for global equities too on the margin.

And this was it for today, thanks for reading!

If you enjoyed the piece, please click on the like button and share it with friends :)

Finally, an important reminder.

From January 1st getting access to this content (and much more!) will require a paid subscription.

On the TMC platform we will step up the game: unique market insights, courses, ETF portfolios, tactical trade ideas, top notch interactive macro tools and much more.

Subscribers to The Long Term Investor tier will get weekly macro insights backed by an ETF portfolio.

On top of that timely macro reports covering live market events and elaborating on tactical trade ideas plus interactive macro tools like the VAMD will be available for subscribers to the All-Round and Pro Investor tiers.

Gates are closing soon: check out which subscription tier suits you the most - I’ll be waiting for you to come onboard!

For more information, here is the website.

DISCLAIMER

The content provided on The Macro Compass newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision. Always perform your own due diligence.

Share this post