‘‘I said that we needed to shift the focus to improving the quality and returns of economic growth, to promoting sustained and healthy economic development, and to pursuing genuine rather than inflated GDP growth and achieving high-quality, efficient, and sustainable development.’’

Xi Jinping, July 2021

China is supposed to become the largest economy in the world over the next decade, and yet it still looks like a black box to many.

By many metrics, investors are still under-allocated to Chinese exposure but arguably there are structural reasons why that’s the case.

So, how does China fit in a global macro portfolio?

In this article, we will shed some lights on China and discuss:

The future of the Chinese cheap-labor and export-based business model, and Xi’s attempts to transition to a new ‘‘common prosperity’’ model;

Whether China is an attractive global macro investment on a medium-term horizon, and why.

Without further ado, let’s jump right in!

How did China get here, and what’s next?

Actually, before we jump right in.

If you are interested in any kind of partnership, sponsorship, or in bespoke consulting services feel free to reach out at TheMacroCompass@gmail.com.

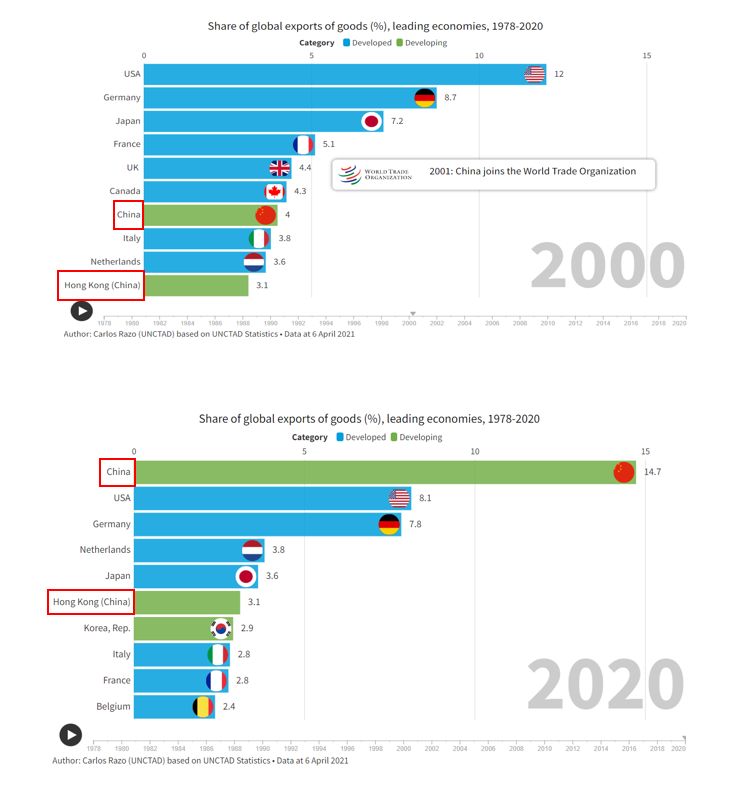

Back to it: China has quickly become a global powerhouse.

Over the last 20 years, the Chinese share of global exports of goods has jumped from 7% to 18%!

But how the heck did they get here and what’s next?

There are 2 sources of growth: structural and cyclical.

Structural, long-term potential growth is mostly driven by the growth in the labor force and total factor productivity trends.

Cyclical growth trends are instead mostly dictated by credit cycles: lever up an economy and you’ll give it a temporary boost, de-lever it and it’s going to be painful.

Over the last decades, China has engineered a tremendous cocktail of both structural and cyclical growth.

Let’s see why, and what’s next.

A) In the last 40 years, Chinese working age population grew from 600 million to >1 billion. That’s a whopping 67% increase (!) in the amount of people that could actively contribute to economic growth.

It’s huge!

As long as you can keep the employment figures on the right track, such a demographics boost is a massive tailwind to structural growth.

(By the way, the chart is from the fantastic Andreas Steno Larsen: must follow on Twitter here and subscribe to his free newsletter here).

But what about future demographics trend?

As you can see, the lagged effect of the one-child policy and the widespread population ageing will take a big toll on the Chinese working-age population over the next decades: in the United Nations medium fertility scenario, the Chinese workforce will shrink from >1 billion now to around 700 million by 2065.

Ouch!

B) Productivity trends have been very favorable especially until 2011, although they have started to stagnate over the last decade.

The chart above shows the estimated Chinese total factor productivity (log-scale) over the last 20 years.

Especially in the early 2000s, as China joined WTO and applied several reforms to reduce external trade and internal migration barriers productivity picked up very strongly (+22% between 2003 and 2011 alone!).

What next, though?

Productivity trends seem to have stagnated a bit over the last decade: WTO tailwinds are behind us and the creation and rapid growth of young Chinese private firms has slowed down. Large-scale and socially ‘‘painful’’ structural reforms would be needed to boost productivity growth going forward.

Effectively, a combination of strong demographics and productivity tailwinds markedly increased Chinese long-run potential (and delivered) GDP growth over the last few decades.

But looking ahead, the structural long-term GDP growth drivers face strong headwinds: the Chinese working-age population is set to materially shrink and total factor productivity growth has lost some steam.

What about cyclical growth drivers?

C) As highlighted, since the early 2010s both demographics and productivity growth started to slow down and so China decided to aggressively overlay cyclical growth with an unprecedented amount of credit expansion in a short period of time.

The chart below shows the total debt (government debt plus the often overlooked private sector debt) as a % of GDP in China against US and EU.

Notice how China took only 10 years (2011-2021) to lever up its entire economy from 170% to almost 300% of GDP.

It took the US and Europe about 30-40 years to achieve the same credit expansion.

Effectively, when structural growth drivers peaked China resorted to large-scale credit creation to boost cyclical growth.

Debt isn’t bad per se: it’s the long-term productivity of newly created credit that determines whether levering up the economy was a profitable exercise or not.

So where did all these Chinese credit creation end up?

Mostly in the private sector: Chinese corporates and households took on large amounts of leverage between 2000 and 2020. Explicit government debt in China isn’t nearly as large as in Western democracies. Why is that the case?

That’s because China has an almost unique feature amongst G10 economies: it can direct credit in almost whatever size, at whatever speed to whatever economic sector they deem fit at any point in time.

This is known as ‘‘(credit) window guidance’’.

The credit window guidance was applied in Japan between the ‘70s and the ‘90s and it’s one of the primary drivers behind the creation of the ‘‘bubble economy’’ of the ‘80s. It consists of a model whereby the central bank would impose bank credit growth quotas on the commercial banks.

Nowadays, China applies a similar model: large, timed and targeted credit injections towards certain sectors via (shadow and commercial) bank lending.

The sheer size of this credit creation over the last decade has led to several asset-prices inflation episodes (primarily in the real estate sector) and to a widening wealth inequality gap: according to Guo Shuqing, the head of the China Banking and Insurance Regulatory Commission (CBIRC), property-related loans were equal to about two thirds of China’s GDP!

What about sustainable common prosperity?!

And indeed, Xi has noticed and things are changing.

The ‘‘new’’ common prosperity and China as a global macro investment

In his famous Qiushi essay in 2021, Xi stressed out that “genuine growth” (as opposed to what he called “fictional growth”) cannot generate enough economic activity to allow China to hit its GDP growth targets: he is well aware of the weakening trend in the Chinese structural GDP growth drivers.

So, what’s the new plan for the Chinese common prosperity?

Reforms.

In 2021, Xi made already clear that the exuberant spirits and ‘‘fictional growth’’ in the tech and real estate sector needed to be curbed (e.g. tech IPO clampdown, the Evergrande saga etc) and resources should be rather allocated to new sources of ‘‘genuine growth’’.

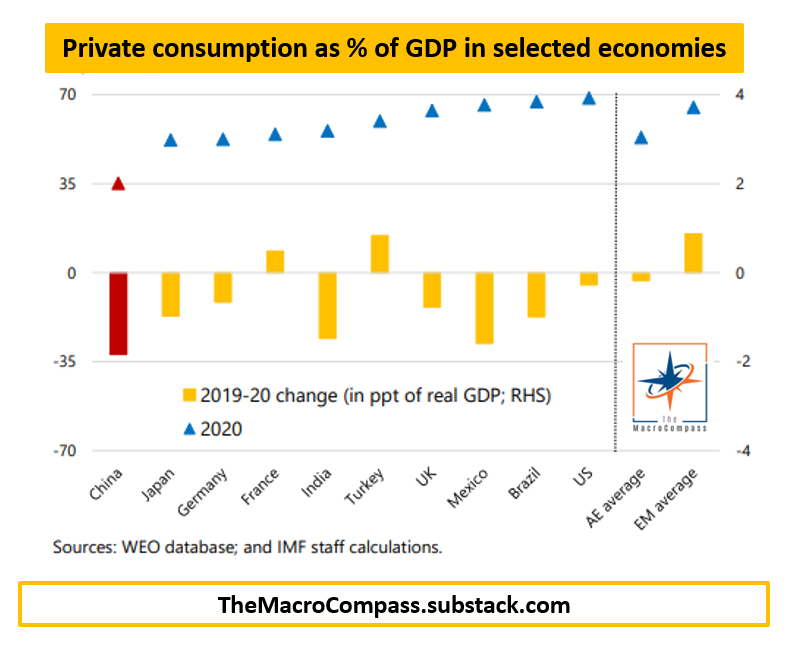

His ambition is to transition the Chinese economy business model from an export-oriented, cheap labor and surplus running country into a domestic demand powered economy that preserves its prominent position as a global exporter.

Well, easier said than done!

In China, private consumption represents only 35% of GDP against 70% in the US and 55% in Germany.

Plenty of room to catch up though, right? In principle, yes.

But in order to boost consumer demand, a larger proportion of economic value-added needs to be redistributed to workers via higher real wages.

But it’s exactly low real wages that have helped China boost its status as a global exporter, and so this transition might prove to be difficult to engineer.

Nevertheless, China holds two competitive advantages:

Xi doesn’t really face a political cycle, and hence he can implement ‘‘painful’’ but useful reforms in a much more effective way vis-à-vis most Western economies;

China is a largely under-owned market from a global portfolio allocation standpoint.

The chart above pictures this under-allocation well: despite China accounting for almost 20% of global population and GDP (in purchasing-power parity terms) and >10% of global exports, it’s equity market cap only accounts for 5% of the global equity markets.

As a friend and great investor would say: there are good reasons for this structural under-allocation, Alf.

How would you feel about arguing against a Chinese company in a Chinese court of law?

Yep, me neither :)

So, what do we make of the Chinese economy and China as a global macro investment?

Conclusions

After weighing all these arguments, I believe China deserves a place in a global macro asset allocation portfolio.

While it’s true that the structural drivers of GDP growth are weakening, the same can be said about most other global economies - but the ability to implement meaningful reforms is arguably much more impaired in Western societies than in China from a political standpoint.

Xi understands the structural headwinds ahead, and he seems committed to engineer more ‘‘genuine growth’’ and transition China from a cheap-labor, export-oriented country to a more domestic-demand centered economy.

The transition is likely to be painful and involve plenty of de-leveraging episodes, and so portfolio allocation should appropriately reflect this expected volatility.

Actually, de-leveraging driven sell-offs could be used as an opportunity to build long-term allocations to Chinese sectors that will benefit from the transition towards a more domestic-driven economy.

The new common prosperity: a bit more common, a bit less prosperity.

Thank you for making it all the way through! :)

If you enjoy my work, I would really appreciate if you could click on the like button at the end of the piece and share the article around.

It would mean the world to me!

For any inquiries, feel free to get in touch at TheMacroCompass@gmail.com.

If you want more macro insights, you can also follow me on Twitter and Linkedin.

See you soon here for another article of The Macro Compass, a community of more than 36.000+ worldwide investors and macro enthusiasts!

Share this post