Hi everybody, and welcome back to The Macro Compass!

We are at that funny phase of the cycle when we look at the most lagging macro indicator (inflation) to assess how late the Fed is going to be this time.

In 2021, a gigantic amount of fiscal stimulus and credit creation led to a red-hot economy and yet the Fed was still doing QE and imposing negative real rates – because you know, inflation was subdued.

As we speak, the economy is growing very slowly and the housing market is frozen.

Still, the Fed is likely to impose 100+ bps positive real rates and QT for much longer than needed while it awaits for the ultimate confirmation that they have damaged the economy for good.

And today’s CPI report sent another clear message in that direction.

To all the disinflationary soft landing cheerleaders out there: forget about it.

In this macro piece, we will:

Have a deep look into the just-released CPI report, assessing its subcomponents according to Powell’s own approach and deriving the likely Fed’s response to these updated inflation figures;

Draw our own conclusions on what this means for macro and markets ahead, with a particular focus on the bond and stock market and considerations on our portfolio strategy.

The CPI Report

How do you analyze inflation numbers?

Easy – like the Fed does.

It might not be the best way to do it, but it’s the only one that matters.

In a speech released a few months ago, Powell told us he divides inflation into three main categories: core goods, housing and services ex-housing inflation.

According to the Fed, this is how things stand:

Core goods are in a disinflationary trend due to the post-pandemic economic recalibration back to services and to much easier global supply chains;

Housing inflation lags what happens on the ground, so it’ll keep increasing for a bit and then start declining in line with much softer asking rents we have seen recently;

Services ex-housing is where they pay most attention and want to see sustained progress to 2%.

Let’s analyze today’s inflation numbers under the Fed’s approach.

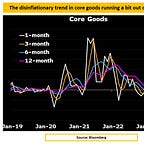

Core goods prices are still in a disinflationary trend, but that powerful impulse seems to be alleviating.

The excessive imbalance between sizeable goods inventories and rapidly declining demand had led to outright core goods deflation (orange and blue lines), but prices seem to be bottoming here.

Nevertheless, freight costs have materially decreased and as shown by the NY Fed the global supply chain keeps normalizing – both positive developments for a continued disinflationary trend in core goods.

Core goods inflation is still looking benign for the Fed, but the disinflationary tailwinds might be alleviating.

Now, to the hot topics: housing inflation, and most importantly Powell’s preferred measure which is Core Services Ex-Housing inflation.

There were important news on both fronts, and the messages coming from the bond market couldn’t be louder.

Let’s dig into it, and assess how medium-term investors should approach such a macro environment…

Getting access to The Macro Compass full-length pieces requires a paid subscription.

On the new TMC platform, you’ll find not only deep and unique macro insights but also ETF Portfolios, tactical trade ideas, interactive tools, and much more.

Come join this vibrant community of macro investors - check out which subscription tier suits you the most using the link below.

For more information, here is the website.