Hey guys! Before we start, an important announcement: welcome to the first piece of the TMC Macro Education Series!

Once a week, I will deliver some bonus educational content covering big picture macro trends, the bond market, monetary mechanics, risk management and more in a quick, 5-min read.

Financial education is a key TMC principle – hence the Macro Education Series is and will always remain FREE.

I hope you enjoy it!

Long-term, structural economic growth is mostly driven by two factors: demographics and productivity.

Both peaked in the late 80s, and we chose to fix the problem with a ton of debt.

It worked until now, but we are at very late stages of the long-term debt cycle.

Healthy demographics and high fertility rates facilitate a growing labor force: retirees are more than offset by new young workers, and hence the share of working-age population as % of total increases.

More workers, more potential for growth.

Over the next decades though, the share of working-age population will decline across many countries: for instance, the Chinese workforce is likely to shrink by 250-300 million people – a hard hit for global growth.

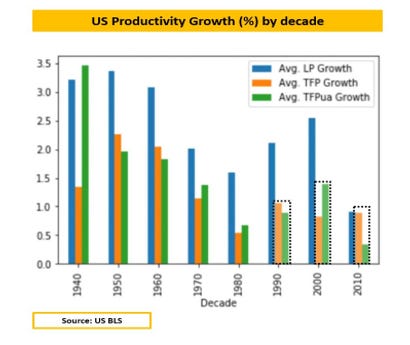

Total factor productivity (TFP) growth measures how productive are capital and labor resources.

Effective capital allocation and technological progress contribute to achieving positive productivity growth.

As the marginal benefit from technological progress declines over time and capital misallocation took center stage over the last 1-2 decades, TFP growth stagnated around 1% per year – not exciting.

As per the early 90s, labor force and productivity growth trends weakened materially.

Potential GDP growth started declining to socially and politically unacceptable levels – so, how did we fix that?

With a ton of debt.

Public + private debt levels as % of GDP amongst developed economies skyrocketed from <200% to over 300% in less than 2 decades, and in China from 100% to 300% in less than 15 years.

Be it mostly through government (Japan) or the private sector (China), credit creation was the ‘’easy fix’’.

To be precise: cheaper and cheaper credit.

Real interest rates relentlessly declined for 3 decades, allowing a system with lower structural growth offset by more and more leverage at cheaper and cheaper borrowing costs to thrive.

The more unproductive debt, the lower real yields must be for the system to survive.

This long-term debt cycle is at its very last innings.

Fighting inflation requires higher real yields, and our over-leveraged system can’t bear that.

And once you deleverage a credit-based system, it’s hard to get it back on its feet.

Just ask Japan.

If you have enjoyed this piece, consider joining The Macro Compass premium platform.

The best investment you can make is in your own macro education, and TMC is trusted by thousands of worldwide investors to deliver unique and actionable macro insights every week.

For more information, here is the website.

Share this post