''The economy of imaginary wealth is being inevitably replaced by the economy of real and hard assets''.

Vladimir Putin, September 2022

Hi all, and welcome back to The Macro Compass!

Last week, Vladimir Putin released a massive speech that clearly outlined his strategy to bring Europe to its knees.

For decades, Europe’s business model has been largely structured around cheap energy and input costs used to produce good-quality manufactured goods to export around the world - Germany being a prime example of such business model.

Due to globalization, ageing demographics and technological advances real output growth wasn’t necessarily spectacular and most importantly interest rates headed lower and lower over time.

This led to another important development: a massive build-up in public and private sector leverage and the hyper-financialization of the West - including Europe.

Putin’s strategy is clear: take away the cheap energy inputs from the equation, and a domino of negative consequences will unfold - economic output will materially suffer, but at the same time energy-driven inflation will roar its ugly head too.

That means that both the real economy and financial markets get squeezed hard: consumers and corporates suffer from negative real wage growth and much weaker profitability, while the highly leveraged ‘‘imaginary wealth’’ economy gets hit by the ECB being forced to tighten financial conditions.

The main question is: will this strategy work, and how will Europe respond?

In this article, we will:

Explore Putin’s strategy in more details: how did Europe get here, and how much leverage does Putin really have?

Summarize the likely European policymakers’ response starting from today’s ECB decision, and conclude with portfolio implications.

Cheap Energy & Imaginary Wealth

''The economy of imaginary wealth is being inevitably replaced by the economy of real and hard assets''.

This single sentence summarizes Putin’s entire strategy designed to try and bring Europe to its knees.

It consists of 3 main points: let’s walk through them.

1. Cheap Energy, Competitive Production, Strong Exports

Once you can get your hands around cheap input costs, manufacture good quality stuff and export it to countries around the world - well, you are looking good.

Germany is the European poster child using this economic model, but many other countries around the world (e.g. Korea) have flourished in the 2000s by relying on it.

The key question is: how important is the ‘‘cheap energy’’ component?

Or in other words: how big is Russia’s economic leverage were they to drastically change this parameter in the equation?

Zoltan Poszar from Credit Suisse calculates that roughly EUR 1.9 trillion of German manufacturing output (red circle in the middle of the chart) relies on only EUR 27 billion equivalent of Russian energy inputs (bottom-left red circle).

That’s quite some embedded leverage.

And what happens to a highly-leveraged environment when the cost or the availability of this leverage (Russian energy in this case) drastically changes?

The system becomes unstable, and because of the embedded leverage the negative reactions are not linear but rather convex.

The chart of the momentum in the German current account balance speaks loud.

Clearly, this strategy aggressively damages Russia too: energy sales to Europe represent a large portion of Russian income, and the second round effect of effectively cutting ties with one of your biggest trading partners are very negative for your domestic economy.

But Putin is planning to go after another important source of leverage, too.

2. Leverage Here, Leverage There, Leverage Everywhere

Putin referred to the ‘‘economy of imaginary wealth’’.

He is talking about the enormous wealth generated through the combination of credit creation and low (real) interest rates Europe has experienced over the last 20 years.

An example?

Extend more mortgages at lower and lower borrowing rates and even if salaries are unchanged, people will be able to ‘‘afford’’ more expensive houses.

Think about it this way: the very same EUR 2k monthly mortgage installment only buys you a house worth EUR 350k at 4% mortgage rates, but if you borrow at 1% you can suddenly ‘‘afford’’ a EUR 500k home - you can quickly become ‘‘wealthier’’ even though your salary or ability to generate long-term cash flows hasn’t changed!

The most common misconception here is that only certain European countries make excessive use of debt.

That’s misleading.

Summing private and public debt, all major European jurisdictions easily exceed 200% of GDP and leading the pack you find France and The Netherlands - not Italy.

And this doesn’t even account for contingent liabilities: those are government guarantees or liabilities of public corporations which aren’t considered in official debt calculations - Germany’s contingent liabilities exceed 100% of GDP (!).

This aggressive credit creation coupled with lower borrowing costs has generated a large amount of financial asset gains - what Putin refers to as ‘‘imaginary wealth’’.

How does he plan to go after this additional source of leverage?

Easy: higher energy costs generate higher inflation, hence forcing the ECB to raise borrowing costs and apply tighter financial conditions - and again what happens in a highly-leveraged environment when the cost or the availability of this leverage (borrowing rates, in this case) drastically changes?

Yep, you get it :)

3. The Release Valves

Now, of course you can’t expect European policymakers to sit back and do nothing.

But do what?

To answer this question, you need to think of this saga like an Emerging Market external shock: EMs business models often depend on certain external inputs to function - a regular flow of USDs, supply of certain goods etc.

Once this input chain is subject to a sharp exogenous shock, the business model breaks and policymakers are faced with challenging short-term decisions that often lead to suboptimal outcomes.

This type of pressure always finds its way to a release valve.

Let’s see where Europe stands: the short-term options are the following.

1) Tighten things up and go through some pain: don’t use government balance sheets (don’t print EUR) to rescue the private sector and convincingly increase real rates (strong ECB hiking cycle) to protect your currency

Release valve: economic growth, highly leveraged sectors and peripheral debt.

The chart below shows an appetizer of what could happen: European high-yield borrowing rates have already doubled (8% now) from their 2014-2021 average (4%) as a result of the foreseen ECB hiking cycle and widening credit spreads.

2) Try to shield the private sector: offset losses by using the government balance sheet (print EUR) while somehow (?!) retain credibility on the inflation-fight front.

Release valve = the currency.

In an EM-like external shock, unfortunately there is no optimal short-term response strategy.

The latest UK and European policymakers’ announcements and today’s ECB meeting clearly signal politicians are going for the second option.

Why, and what does it imply?

The European Policymakers’ Response & Portfolio Implications

Today’s most important ECB announcement was not the 75 bps hike.

Instead, it was the sneaky wink to European excess liquidity and the banking sector.

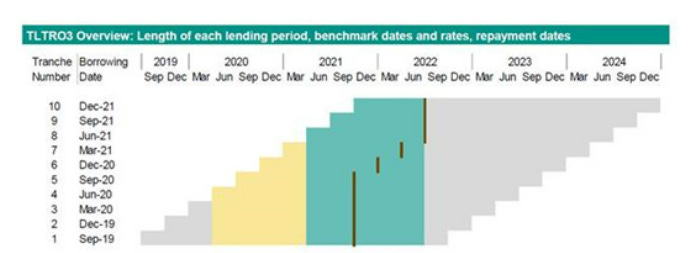

In 2020-2021, European banks borrowed more than EUR 2 trillion from the ECB via the so-called TLTRO operations.

The borrowing conditions were extremely advantageous with interest rates as low as -1% for the Jun20-Jun22 period and after that equivalent to the average ECB deposit rate throughout the lifetime of the TLTRO operation.

Please notice: that’s the average between -50 bps (ECB depo until Jun22) and the new prevailing ECB depo from now onwards.

Now, there are roughly 2 more years to go before these TLTRO loans mature but banks could in principle opt to repay early - hence reducing the ECB balance sheet.

Today, the ECB gave a nice incentive to banks NOT to repay these loans though:

The funding costs are low: they were locked for Jun20-Jun22 at -1% for basically all banks, and going forward they will be equivalent to the average ECB depo rate between Jun22 and the maturity of the TLTRO loan.

Looking at market-implied forwards, that means roughly 25/50 bps borrowing costs ahead.But on the investment side, banks will be making good money: if they merely park the excess reserves they borrow back at the ECB, according to the same market-implied forwards they will be making on average 125/150 bps!

With such an incentive schemes, it’s very likely European banks won’t be repaying these loans. There was also no mention of QT discussions at all.

This means the ECB balance sheet won’t shrink, and EUR excess liquidity won’t be coming down anytime soon.

This has to be seen in the context of European governments announcing guarantees and outright help to the private sector during the energy crisis: in other words, the public sector will be absorbing losses through its balance sheet - which means printing more EUR via deficits.

What does it mean for European assets?

While more real-economy EUR being created (deficits) and persistently high financial-economy EUR balances (bank reserves) could be net positive for the private sector through less defaults and a smaller decline in earnings, the EUR is poised to act as a long-term release valve.

The European policymakers’ response complicates Putin’s agenda as it buys Europe some time to find medium-term solutions to the energy crisis while the Russian economy continues to face challenging economic conditions.

But in any case, Europe has suffered a structural hit.

Long-term investors will be doubting the future viability of the good old European business model and the EUR will be serving as a pressure release valve for some time.

I remain tactically short EUR/USD and structurally cautious on European assets.

And this was all for today, thanks for reading!

If you are interested in any kind of partnership, sponsorship, conferences or media appearances feel free to reach out at TheMacroCompass@gmail.com.

Finally: may I ask you to be so kind and click on the like button and share this article around, so that we can spread the word about The Macro Compass?

It would make my day!

See you soon here for another article of The Macro Compass, a community of more than 91,000+ worldwide investors and macro enthusiasts!

For more macro insights, you can also follow me on LinkedIn, Twitter and Instagram.

Feel free also to check out my new podcast The Macro Trading Floor - it’s available on all podcast apps and on the Blockworks Macro YouTube channel.

For any inquiries, feel free to get in touch at TheMacroCompass@gmail.com.

DISCLAIMER

The content provided on The Macro Compass newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision. Always perform your own due diligence.