The US is dangerously close to triggering its debt ceiling limit, and yet markets seem very relaxed.

The 2011 episode shows us how political incentive schemes can instead drag negotiations until the very last minute, and force investors to price in a more meaningful probability of an actual bad outcome.

So, let’s have a look at:

The actual mechanics of government spending and the meaning of a debt ceiling;

The potential x-date and what happens if we cross that without a deal;

The impact on bonds, equities, and the US Dollar under a no-deal scenario.

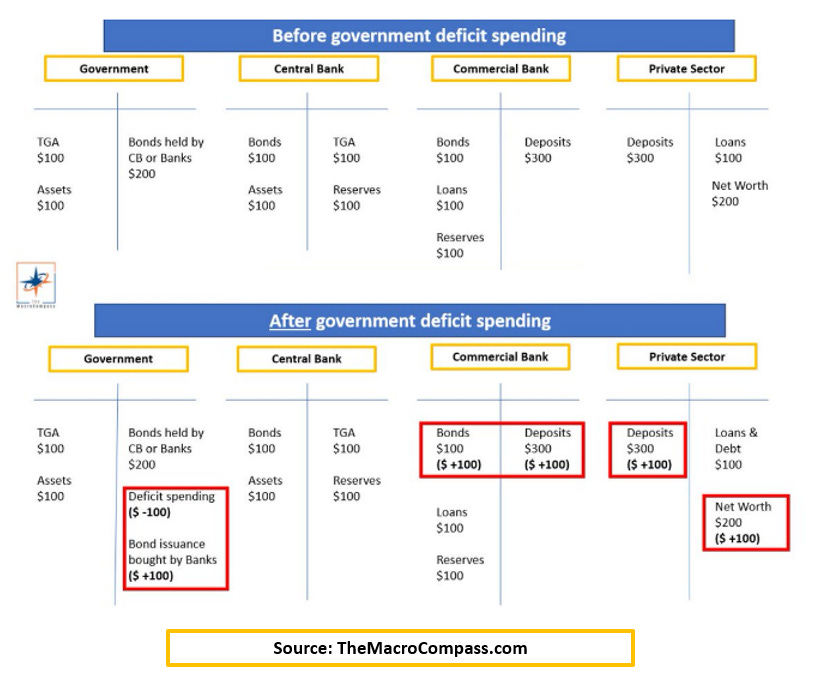

In our monetary system, the government doesn’t need money to spend money.

As the very issuer of the currency we use, with deficit spending the government actually increases our net wealth – for instance, tax cuts imply we have more spendable money without incurring in any direct liability.

The real limitation to uncontrolled deficit spending is not ‘’where is the government going to find money’’, but inflation: excessive deficits may lead to (unproductive) excess demand which often can’t be met by a rapid increase in supply or resources – and the release valve is then an ugly inflationary spiral.

In any case, we also have another self-imposed accounting rule which dictates the government can’t run with negative equity and hence must issue bonds to ‘’fund’’ its deficit spending – see the table below.

This is when the US debt ceiling becomes a problem: another self-imposed limitation which prevents the US from incurring in debt above a certain threshold to ‘’fund’’ its deficit spending.

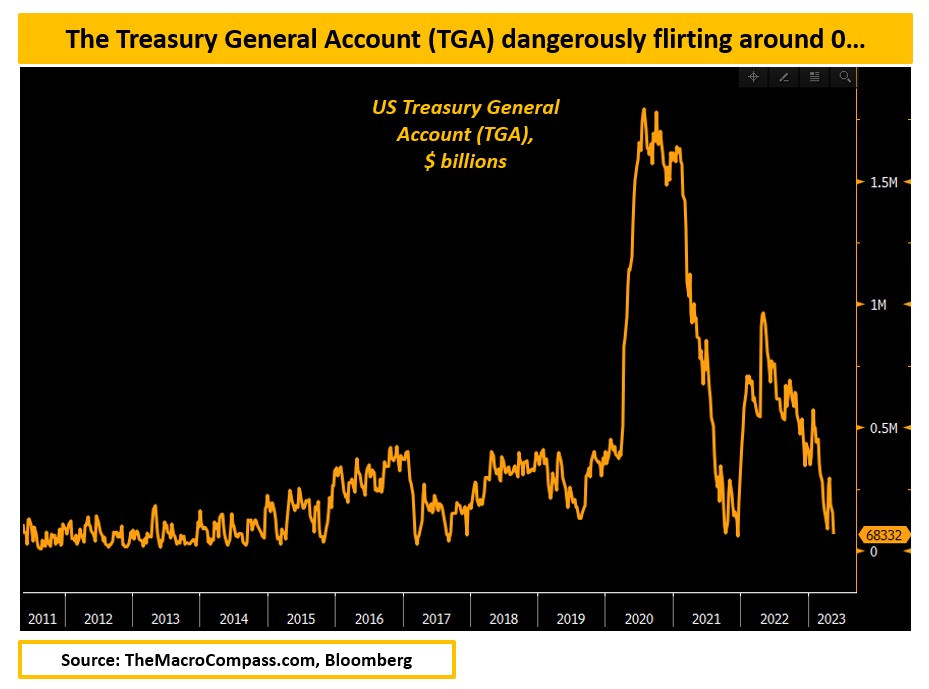

If the government can’t issue bonds anymore, to maintain its current level of (deficit) spending it will spend down its Treasury General Account at the Fed – but we are running out of fuel there too.

The TGA has been rapidly drawn down from $600 billion in January to less than $70 billion as per last week.

A key question is – when do we actually hit the zero lower bound?

John Comiskey (here) has been doing a great job in tracking and estimating government cash flows to project the famous ‘’x-date’’ when the US government is going to empty its TGA completely.

His latest analysis shows that between Jun 2nd and Jun 9th we are going to be dangerously, dangerously close to the zero lower bound – and as Yellen already warned us, we might actually hit it around these dates.

It’s worth remembering that past these dangerous dates, by Jun 12th new tax receipts would be coming in hence providing a much needed TGA boost to the government.

But let’s assume the TGA hits zero and the debt ceiling prevents the US government from issuing bonds to fund (deficit) spending.

Would the US government default then?

What would be the impact on bonds, stocks, the US Dollar and Gold and are markets preparing for such an outcome or would they be surprised?

How to prepare a portfolio for such an outcome?

Let’s dig in…

Eager to read the remaining part of this macro report?

Come join The Macro Compass premium platform to get access to Alf’s full-length timely pieces, actionable investment strategy and much more!

Check which subscription tier suits you the most using this link or the button below:

For more information, here is the website.

Share this post