Hi everybody, and welcome back to The Macro Compass!

Most macro commentary focuses on the US.

But over the last few months, the real golden kid has been Europe.

Recently the EUR has appreciated 10%+ against the US Dollar, macro data seems to suggest a recession has been avoided and the European stock market is on a roll having outperformed the S&P500 and other peers.

For foreign macro practitioners, the complex European architecture and its many dimensions appear like an unattractive black box to analyze.

This is why in this piece, we will:

Discuss the main drivers behind the recent European macro and market outperformance;

Answer the big question: where do we go from here?

September 2022.

European stock markets in free fall, EUR/USD at 0.95 – will Europe be able to keep its lights on this winter? These worries were justified by the complex macro and energy picture back then.

But while not good at long-term policymaking, Europe is great at avoiding last-minute disasters.

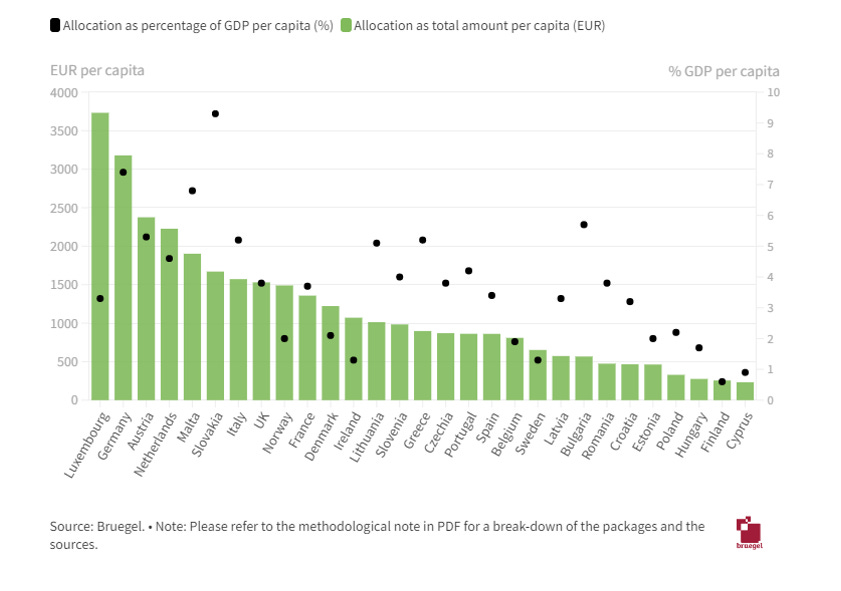

The chart above shows the gargantuan amount of GDP per capita allocated by different European countries to households and firms in an attempt to fight the energy crisis.

On average, countries allocated ~5% of GDP per capita against the energy crisis: that’s a huge figure.

To put it in context, an entire year’s Italian fiscal deficit ranges about EUR 50-60 bn and Italy allocated over EUR 90 bn (!) solely to shield consumers and firms from higher energy prices. Wow.

Again, Europe is bad at long-term policymaking but good at emergency measures.

Using public finances to shield the private sector from a structural trade/commodity problem isn’t a viable long-term solution, but it sure works in the short term because it fixes terms of trade.

What’s that?

Terms of trade indices measure the relative performance of a country’s export and import prices.

Better (higher) terms of trade = the value you get out of your exports is outperforming the value of the stuff you need to import from outside, and vice versa.

Terms of trade are important for the currency: deteriorating/improving ToT often involve a weaker/stronger currency since the country has to spend more/less to import the same amount of products.

I mean, this chart is quite telling: as soon as Europe massively intervened and terms of trade (orange) started improving, the EUR caught a relentless bid.

A stronger EUR and better sentiment underpinned the recovery in European risk assets too, but the kicker was that government intervention also killed the recessionary vibes.

The extreme pessimism around the manufacturing industry was now less justified as input and energy costs were subsidized by governments, and so an immediate earnings recession had to be priced out.

European stocks staged a massive rally and outperformed many global peers.

On top of it, soft macro data started validating this new narrative as PMI surveys saw more optimistic answers about future economic growth.

This begs the question: where do we stand now, and what’s ahead for Europe?

The chart below is an eye-opener…

Enjoyed it so far and eager to read the remaining part of this macro report?

Come join The Macro Compass premium platform to get access to Alf’s full-length timely pieces, actionable investment strategy and much more!

This piece is reserved to All-Round Investor subscribers - check out the product clicking on the button below.

For more information, here is the website.

Share this post