Hi everybody, Alf here - welcome back to The Macro Compass!

Before we go into today’s piece, a short announcement.

I advise several institutional investors on a bespoke basis.

Clients include Canadian pension funds, one of the biggest tech companies around, and top 3 multimanager hedge funds in the world.

Services go from sitting on the investment committee as an independent advisor, to constructing specific macro portfolios/hedging programs and consulting on a day-to-day basis (i.e. act as their independent macro analyst).

Are you are interested in my macro advisory services?

Please shoot an email with your request at: alf@themacrocompass.com

Fair warning: it’s not cheap, and it’s only for institutional investors.

Now, to the piece.

The first 5 weeks of the year have seen international equities outperforming the S&P 500: European and Chinese stocks have rallied harder than US stock indexes, and certain emerging markets like Chile or Poland are doing even better.

My main thesis for the first half of the year remains to be positioned with an ‘’International Risk Parity’’ portfolio: long US bonds, and long stocks around the world.

Let’s take a look at why.

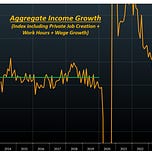

The chart above shows that the US growth exceptionalism might be over.

The Aggregate Income Growth series is a great proxy for nominal growth in real time: it includes private sector job creation, workweek hours, and wage growth – effectively reflecting the growth rate of nominal income US workers are bringing home.

Today, it sits at 4.5% which is exactly the average level it recorded in 2014-2019.

These are the Goldilocks growth conditions and controlled inflation that international stocks enjoy.

Let’s now perform a data-driven analysis of what asset classes perform best during this prevailing macro conditions, and specifically when:

Core inflation is in the 1.75-2.25% range;

Real growth is in the ~1.50-2.50% range.

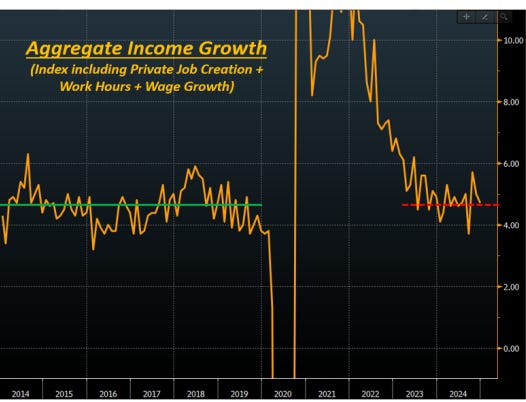

Here is what we found:

On a risk-adjusted basis, bonds do well - especially the long-end.

Stocks perform well too, with international stocks performing slightly better than US stocks: in our sample, European stocks pop up very often with CEE countries (higher beta like Romania or Hungary) leading the table.

To do well, international stocks need a combination of:

Goldilocks growth conditions (no US exceptionalism);

(On the way to be) controlled inflation and predictable Central Banks;

Reasonable valuations and a new narrative replacing the existing stale one.

Which brings us to the other required conditions: friendly developments in inflation coupled with a reasonable Central Bank, cheap valuations and a new narrative prevailing.

What are the best countries to look at today?

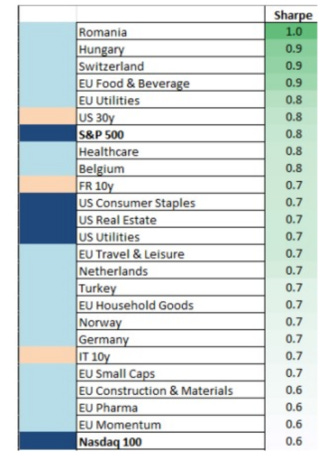

Let’s have a quick look at valuations:

The table above shows the forward P/E ratio for various international equity markets, and the most right column shows the 10-year percentile of valuations.

Broader European equities are still reasonably valued (Stoxx 600 more than Stoxx 50 which tends to give more focus to large cap German and French companies), but the standout country remains Poland.

Outside Europe, several countries in Asia and LatAm show cheap valuations.

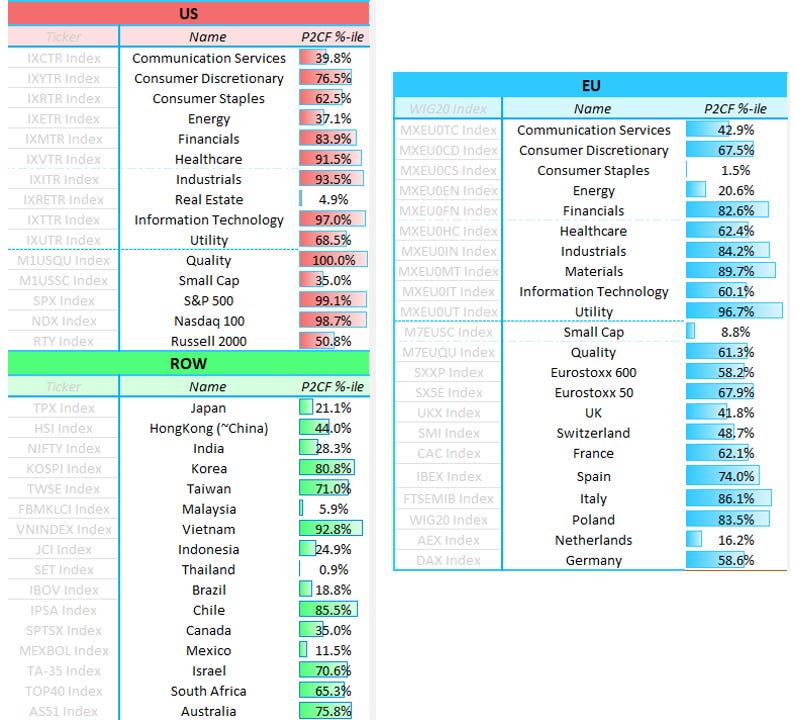

Price-to-earnings ratios alone are not enough as a metric for valuations, and to broaden up the valuation assessment I like to look at Free Cash Flow Yield too.

FCF yield is the ratio between free cash flows and enterprise value, and you can think of it a measure of the amount of net cash genetated by the company and literally available to stock investors divided by the enterprise value.

The table below shows the 10-year percentile of FCF yield for different US and EU sectors, and different stock indexes around the world - the lowest the percentile, the cheaper the valuation:

If you consider valuations, policymaking and narratives my shortlist for international equity markets includes:

Developed markets: Europe, Japan, and Canada

Emerging markets: China and Mexico

Europe, Canada and Mexico were ‘‘priced to die’’ under the tariff threat, but as time goes by without much being done there investors are slowly realizing that inflation is under control and Central Banks are acting dovish. That supports stock markets.

In Japan, valuations are still broadly attractive because investors are growing nervous on how hawkish the BoJ will be - yet nominal growth is doing great (~5%+) and Ueda already verbally intervened to put a cap on bond yields.

Strong nominal growth and a cap on excessive tightening will benefit Japanese stocks.

Despite the big rally, Chinese stocks are still reasonably priced - the PBOC remains ready to ease, some fiscal spending is happening, and investors are largely underallocated.

In short: our analysis suggests that an ‘‘International Risk Parity’’ portfolio built with long US bonds and long international equity markets will perform well in H1 2025.

Thanks for reading!

If you enjoyed this piece, please share it with a friend:

Before you go, don’t forget this.

I advise several institutional investors on a bespoke basis.

Clients include Canadian pension funds, one of the biggest tech companies around, and top 3 multimanager hedge funds in the world.

Services go from sitting on the investment committee as an independent advisor, to constructing specific macro portfolios/hedging programs and consulting on a day-to-day basis (i.e. act as their independent macro analyst).

If you are interested in my macro advisory services, please shoot an email with your request at alf@themacrocompass.com

Fair warning: it’s not cheap, and it’s only for institutional investors.

Share this post